ESRS reporting is more than checking boxes, it’s a tangible financial asset. By standardizing your ESG data, you reduce investment risk, lower your cost of capital, and uncover operational efficiencies that boost your bottom line.

Turn your sustainability data into valuable insights

Meet investor and customer demands

Future-proof your business against regulatory change

Use ESRS to prove your value and outpace the competition

Go beyond compliance

ESRS gives organizations a holistic ESG framework that supports better business decisions with a structured view of sustainability performance.

Unlock strategic insights

Double materiality and standardized metrics help identify ESG risks and opportunities across the value chain—supporting priorities like climate resilience and workforce stability.

Build credibility

Comparable data strengthens stakeholder confidence, reinforces brand trust, and prepares organizations for future regulatory expansion.

“We didn’t want to mix and match different systems for ESRS and carbon accounting. Position Green provided an integrated solution that covered both, which was a huge advantage.”

Andreas Liese, Global Head of Sustainability and Corporate Compliance at PolyPeptide

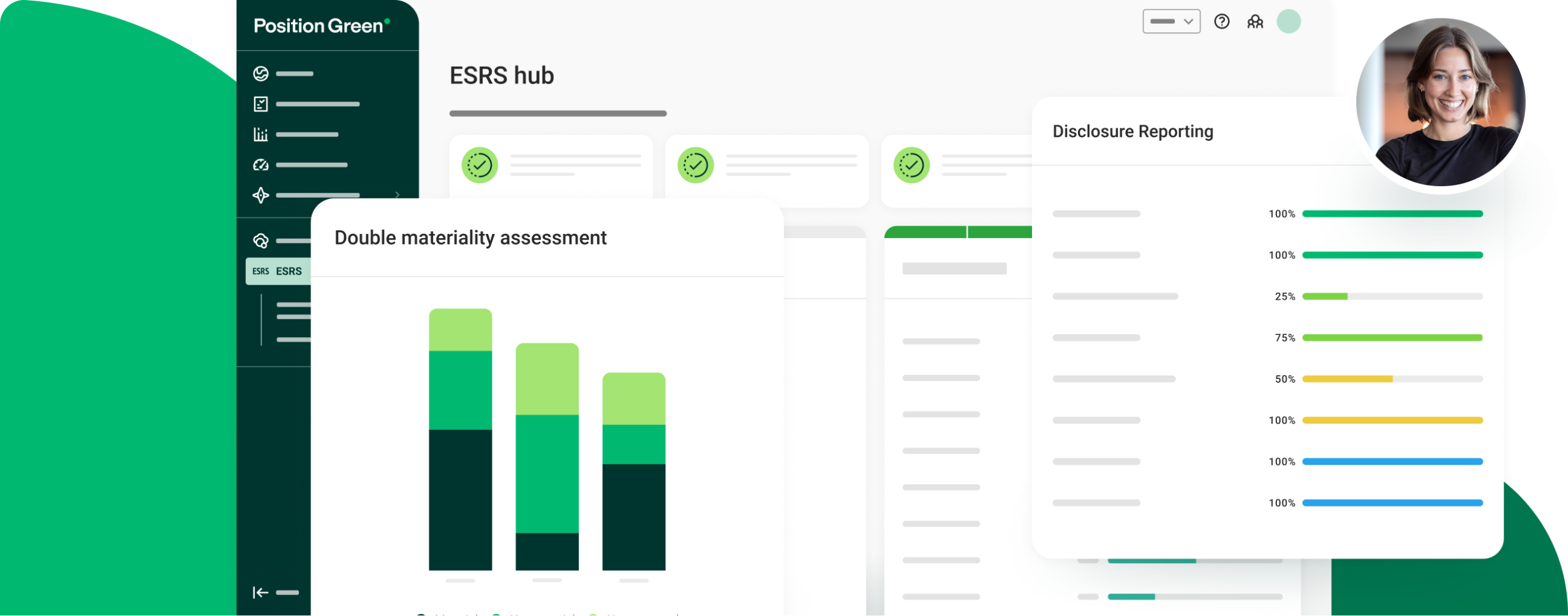

Our platform turns ESRS reporting into a business asset

Built for ESRS, from materiality to statement

Our platform covers the full ESRS journey, without spreadsheets or patchwork tools. We help sustainability, finance, and compliance teams move faster with confidence.

Conduct a Double Materiality Assessment (DMA) aligned with ESRS

Use ready-made ESRS reporting templates

Create a complete, audit-ready sustainability statement

AI-powered reporting, with humans in control

Automation accelerates ESRS reporting, but governance remains essential. Our AI capabilities reduce manual effort while preserving transparency and accountability.

Upload documents and let AI pre-fill ESRS data

Gain full visibility and traceability into AI suggestions

Create approval workflows and consolidated sustainability statements

ESRS experts ready to lend a hand

Whether you’re starting from scratch or scaling your strategy, our in-house sustainability advisors are ready to lend their expertise when you need it.

Get an expert review of your draft sustainability report

Translate reporting requirements and strategy into a clear wireframe

Streamline your reporting through integrations and automations

Driving measurable results at scale:

70%

Faster ESRS reporting YoY

50%

reduction in manual admin

0%

Spreadsheet dependencies

100%

Transparent audit trail

Cut the time spent on ESRS reporting

Automate repetitive tasks and streamline your entire reporting process

Why should enterprise companies invest in ESRS reporting beyond compliance?

ESRS provides decision‑grade ESG data that supports risk management, capital allocation, and long-term strategy—far beyond meeting regulatory requirements.

How does ESRS reporting help CFOs and finance teams?

Standardized, auditable ESG data improves financial risk assessment, supports investor disclosures, and aligns sustainability performance with financial planning.

What makes ESRS different from previous sustainability frameworks?

ESRS introduces legally binding, detailed, and comparable standards—anchored in double materiality—creating a consistent ESG baseline across Europe and beyond.

How does ESRS reporting improve enterprise risk management?

By systematically identifying material ESG risks and opportunities, ESRS strengthens resilience across climate, supply chains, workforce, and governance.

Can ESRS reporting scale across large, complex organizations?

Yes. With the right platform, ESRS reporting can be standardized across entities, regions, and data sources—without increasing manual workload.

How does your platform ensure data quality and audit readiness?

We provide traceability, validation checks, expert guidance, and approval workflows—ensuring ESG data stands up to internal and external scrutiny.

How does ESRS prepare organizations for future regulations?

ESRS establishes a structured ESG data foundation that can be reused as regulations expand globally—reducing future compliance costs and complexity.