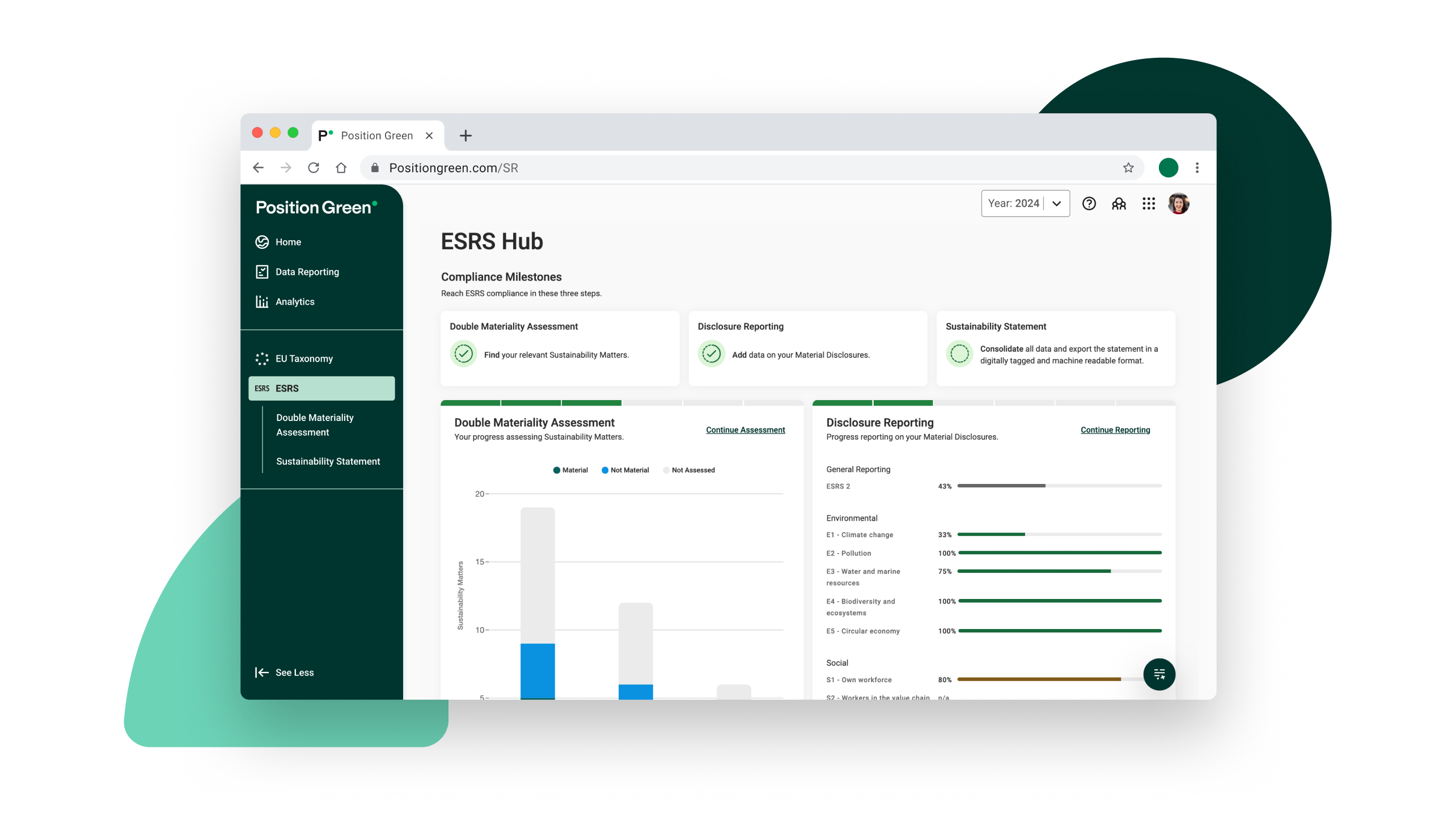

The Corporate Sustainability Reporting Directive (CSRD) is an EU standard intended to make corporate sustainability reporting more standardised and consistent, requiring eligible companies to produce annual sustainability reports. The new European Sustainability Reporting Standards (ESRS) are a central element of the CSRD and specify how and what information and metrics companies must report to comply with the CSRD.

Reporting according to the ESRS is mandatory for all companies covered by the CSRD and must be incorporated in the management report. The reporting standards will also require companies to pay even more attention to traceability and transparency throughout the reporting process due to the limited assurance requirement.

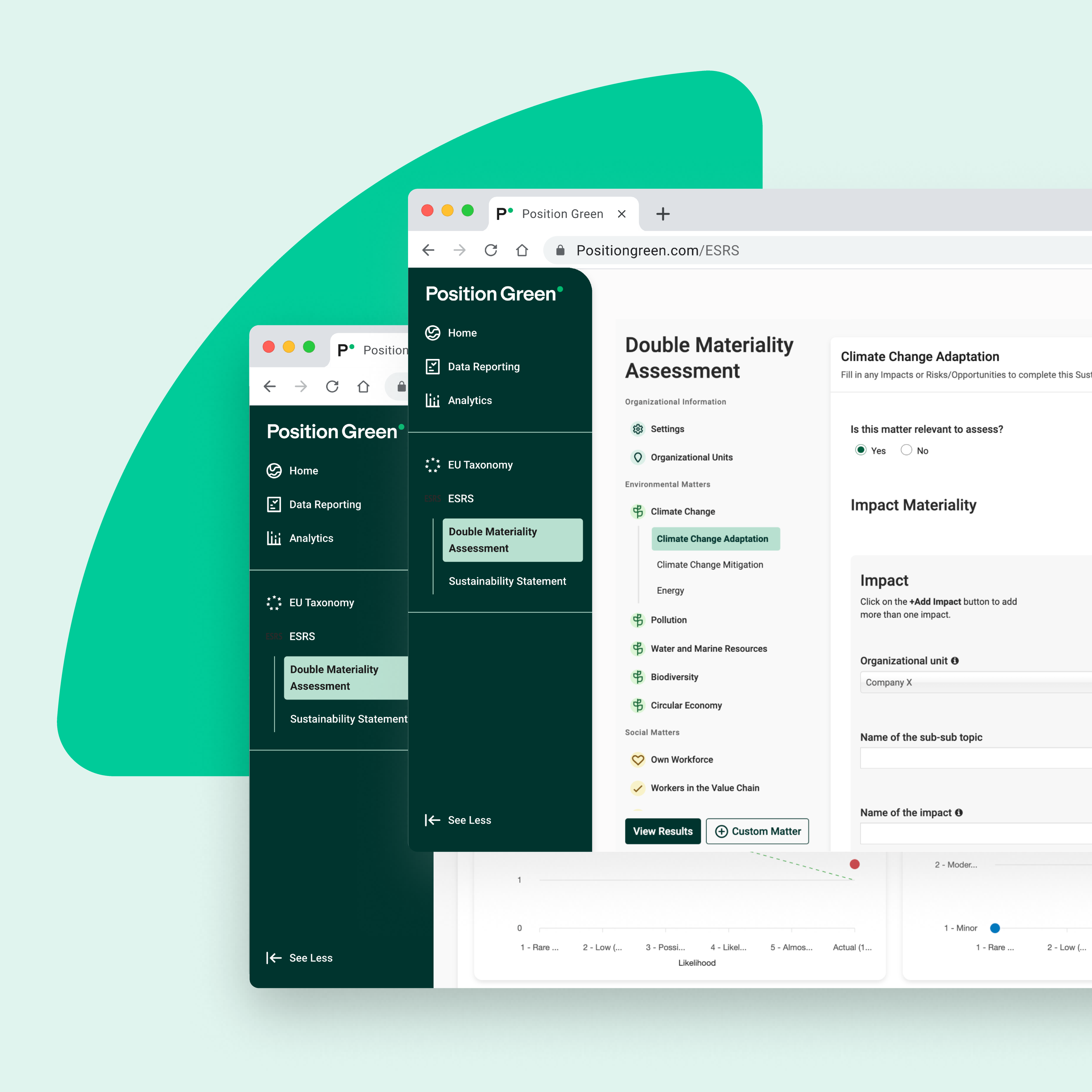

The ESRS have a broader view of materiality than, for example, GRI Standards, and they are based on double materiality from an impact and financial perspective. The double materiality assessment will help companies to understand their impact, risks and opportunities spanning across their upstream and downstream value chains, arising from business relationships, geographical locations and more.