How the simplified ESRS changes the DMA process and informs strategic compliance

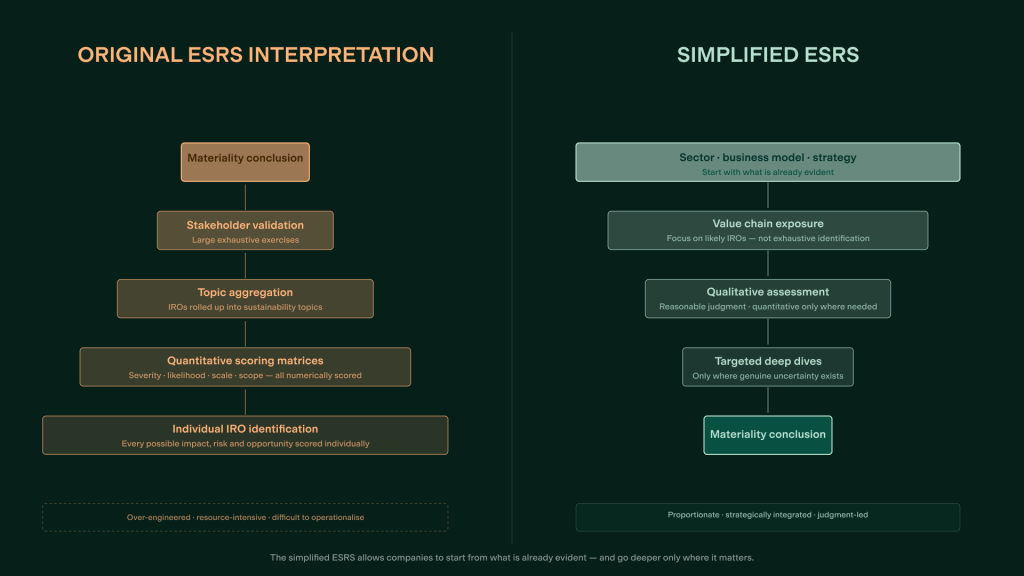

Under the original ESRS, many organisations interpreted the DMA as an exhaustive exercise requiring highly granular assessments across every sustainability topic, value chain segment, and potential impact, risk, or opportunity. In practice, many first-generation DMA methodologies evolved toward highly granular approaches as organisations worked to align with the original ESRS expectations around comprehensiveness, value chain coverage, and defensibility.

The amended ESRS introduces more methodological flexibility and greater proportionality. Alongside it, companies now also have a new approach to the DMA. To be clear, the simplified ESRS does not remove the double materiality assessment.

Companies now have more freedom to determine how materiality conclusions are reached, provided those conclusions remain reasonable, supportable, and capable of supporting a fair presentation of material sustainability topics.

Importantly, this is not simply a simplification, but rather a strategic reframing of the DMA itself. The updated guidance on DMAs is more aligned with original materiality assessments or risk assessments, making it more aligned to what you would originally use to determine risks and opportunities.

This new process has the potential to become less of a compliance-heavy reporting exercise and more of a practical prioritization tool tied to operations, risk exposure, capital allocation, and business strategy, with some key nuances worth highlighting.

The DMA remains the backbone of ESRS reporting

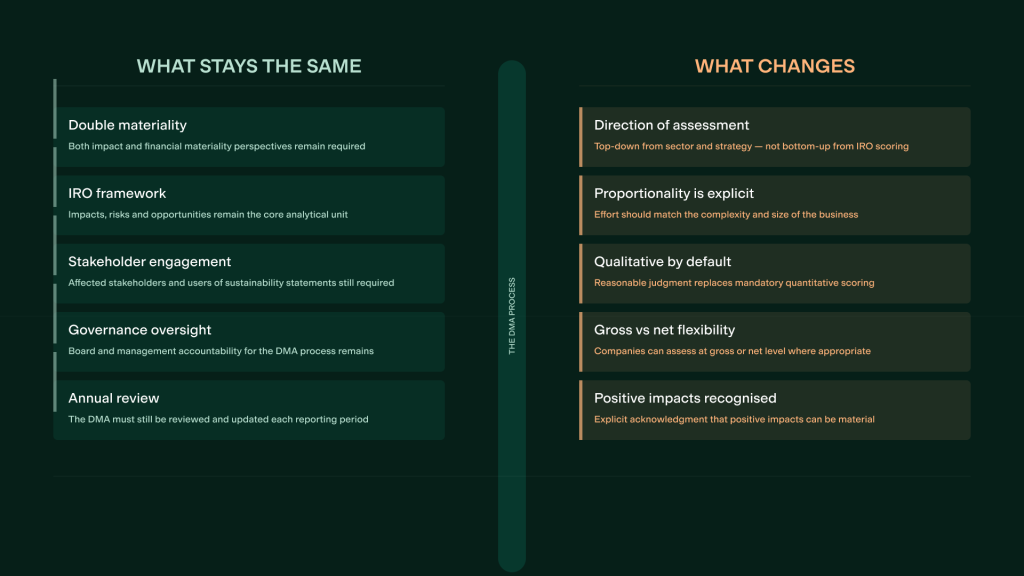

One of the most important points in the simplified ESRS is what has not changed. Double materiality remains central to the ESRS framework. Companies still need to assess:

- Sustainability impacts on people and environment

- Sustainability-related financial risks and opportunities

- Material topics requiring disclosure

The simplified ESRS does not replace the DMA with a checklist approach, nor does it remove the need for judgment, evidence, or governance. Instead, the changes primarily affect:

- How materiality can be concluded

- How much evidence is required

- How exhaustive the process must be

- How companies document their reasoning

In line with this, we now have more guidance on the interpretations of things like positive impacts and gross versus net risk, meaning you have a firmer understanding of the methodology of the DMA, as much as its purpose.

This shift reflects how many organizations and advisory teams operationalized the original ESRS guidance conservatively in order to ensure methodological rigor and defensibility. The revised framework moves closer toward proportionality and reasonable evidence thresholds.

What changed in the simplified DMA process?

1. Companies can now use a top-down DMA approach

This is arguably the most significant methodological shift. The amended ESRS explicitly allows companies to conclude that a topic is material based on sector exposure, business model characteristics, strategy, or value chain realities — without first conducting exhaustive bottom-up assessment of every individual impact, risk, or opportunity (IRO).

This is referred to as a “top-down” DMA approach. Under earlier ESRS interpretations, many DMA methodologies emphasized highly granular documentation in order to align with expectations around completeness and defensibility.

The revised framework allows the reverse logic. For example:

- A mining company may reasonably conclude that biodiversity is material based on sector exposure alone.

- A global manufacturing company may conclude climate transition risk is material without individually scoring every possible climate-related IRO.

- A labour-intensive business may conclude workforce topics are material based on workforce profile and operating model.

- A software company with limited physical operations, low environmental footprint, and minimal exposure to resource-intensive supply chains may reasonably conclude that water and marine resources are not material after a top-down assessment of its business model and value chain exposure.

The amended ESRS also allows companies to combine approaches, top-down for some topics, bottom-up for others. This creates much more flexibility operationally, as you not only get to dismiss wholly immaterial areas of materiality, but define your best business practices for assessing what is.

Strategic implication: focus effort where deeper analysis adds value

For mature organizations, this change could significantly reduce unnecessary process complexity. Under earlier DMA interpretations, some companies spent substantial time documenting highly granular assessments for topics that were already evidently material based on sector exposure or operational realities. The revised approach allows organizations to focus deeper analysis where uncertainty genuinely exists. That means:

- Less time scoring obvious topics

- More time understanding operational exposure

- More room to use the DMA strategically rather than mechanically

For example, a pharmaceutical company may still need detailed bottom-up assessment for access-to-medicine impacts or product governance, but climate, workforce, or business conduct topics may already be sufficiently evident through top-down assessment. The DMA becomes more useful when organizations focus effort where business judgement is actually required.

2. The ESRS no longer expects exhaustive identification of every possible IRO

Another major change involves proportionality. The amended ESRS states that companies are not required to assess every possible impact, risk, or opportunity across all topics and value chain areas. Instead, assessments should focus on likely IROs based on:

- Sector

- Business model

- Strategy

- Value chain exposure, using “reasonable and supportable information available without undue cost or effort”

This language matters operationally. Many first-generation DMA exercises became highly resource-intensive as organisations and advisors worked to operationalize the original ESRS expectations around comprehensiveness and value chain coverage. The revised wording moves closer to traditional enterprise risk methodologies:

- Prioritize likely exposure

- Rely on reasonable evidence

- Avoid unnecessary procedural overload

The framework also clarifies that companies do not need to conduct exhaustive searches for information if reasonable evidence is already available.

Strategic implication: integrate the DMA with existing risk processes

This change creates a major opportunity for organizations to integrate sustainability materiality more closely into existing governance structures. Rather than treating the DMA as a standalone sustainability exercise, companies can increasingly align it with:

- Enterprise risk management

- Procurement risk assessments

- Operational due diligence

- Compliance frameworks

- Strategic planning processes

Organizations with mature operational risk functions may already possess much of the evidence required to support DMA conclusions. That can significantly reduce duplication across sustainability teams, procurement, finance, compliance, and operations.

3. Qualitative assessments now play a larger role

The simplified ESRS explicitly states that qualitative analysis may be sufficient in many cases to conclude on materiality. Quantitative scoring is no longer implicitly expected everywhere.

Many early DMA methodologies incorporated detailed numerical scoring models to support consistency, auditability, and methodological rigor under the original guidance. In practice, many of those scoring models created a false sense of precision. The revised ESRS places greater emphasis on reasonable judgement supported by evidence rather than purely numerical methodology.

Companies must still assess severity, likelihood, scale, scope, and irremediability where relevant, but the framework now gives organizations more freedom in how they arrive at conclusions.

Strategic implication: better executive engagement

This change may also improve internal usability of the DMA. Highly technical scoring systems often became difficult for boards and operational leaders to engage with meaningfully. Materiality discussions sometimes drifted toward methodology debates instead of strategic decision-making.

A more qualitative and judgement-based process can help companies focus on operational exposure, discuss strategic implications more clearly, and improve executive ownership of sustainability priorities. The DMA becomes more useful when leadership teams can understand and challenge conclusions without needing to decode complex scoring matrices.

4. Gross versus net assessment becomes more flexible

The amended ESRS also introduces greater flexibility around considering mitigating actions and controls when assessing impacts, risks, and opportunities. Under the revised framework, implemented actions and controls can influence the assessment of risks and impacts, particularly for potential impacts and risks.

The example included in the DMA guidance illustrates this through wastewater pollution in textile manufacturing. A company implementing stronger chemical management, wastewater treatment systems, supplier controls, and monitoring mechanisms may reduce the likelihood, scale, scope, and irremediability of impacts.

This creates a more operationally realistic methodology. Earlier DMA methodologies often assessed impacts conservatively in order to ensure consistency and avoid understating exposure under the original guidance. The revised approach better reflects how risk assessment functions typically operate inside businesses.

Strategic implication: demonstrate governance maturity

This change creates incentives for stronger operational controls and governance systems. Organizations with mature supplier oversight, environmental controls, due diligence systems, and mitigation processes may now be better positioned to demonstrate reduced exposure across certain risks and impacts.

That creates a closer relationship between operational governance, risk reduction, and sustainability reporting outcomes — making the DMA less theoretical and more connected to actual management performance.

5. Positive impacts are now defined much more narrowly

The amended ESRS also tightens the definition of positive impacts. Simply complying with regulation, preventing harm, or mitigating negative impacts does not automatically qualify as a positive impact.

The guidance specifically notes that activities such as anti-corruption programs, paying adequate wages, workforce training, and transparent tax reporting are generally no longer considered positive impacts on their own. Instead, positive impacts must involve genuinely beneficial outcomes beyond baseline responsibility. Examples provided include enabling the green transition, improving food security, disaster relief support, and reducing chronic disease.

Strategic implication: less sustainability inflation

This change pushes organizations toward more credible sustainability narratives. Under earlier reporting cycles, some companies categorized standard governance or compliance activities as “positive impact,” which often weakened the quality and credibility of disclosures.

The revised approach creates clearer separation between responsible business conduct, risk mitigation, and genuinely positive contributions. That should improve comparability, reporting credibility, and investor usability over time.

What remains unchanged?

Despite the methodological flexibility introduced, several core principles remain firmly intact. Companies still need to ensure fair presentation, faithful representation, neutrality, completeness, and verifiability. The DMA still needs to support sustainability reporting that is complete, neutral, accurate, understandable, and evidence-based.

The revised framework does not eliminate accountability for judgement. In fact, greater flexibility arguably increases the importance of clear rationale, documented assumptions, and defensible methodology choices. Organisations now have more freedom, but also more responsibility to explain why conclusions were reached.

The DMA is becoming more strategic

Perhaps the biggest shift in the simplified ESRS is not technical. It is organizational.

The revised ESRS creates more room for organizations to align the DMA with broader operational risk management, governance, and strategic planning processes. The most useful DMA processes will likely be those that:

- Integrate with operational risk management

- Align with strategic planning

- Support procurement and value chain oversight

- Improve visibility into long-term exposure

The organisations likely to benefit most from the revised ESRS are not necessarily the ones performing the largest assessments. They are the ones using the DMA to clarify priorities, improve operational visibility, strengthen resilience, and support better long-term decision-making.

Get ahead of the changes so you can focus on strategy

Our team of in-house advisory experts and software specialists are already helping businesses adapt their sustainability work to fulfil compliance needs and orient themselves for more strategic due diligence. Whether you are pursuing the full ESRS requirements or want to align to the latest amended ESRS, we can help you chart a course that makes sustainability just good business.

Chat with us

Maja Bjuggstam

Senior Associate

Position Green