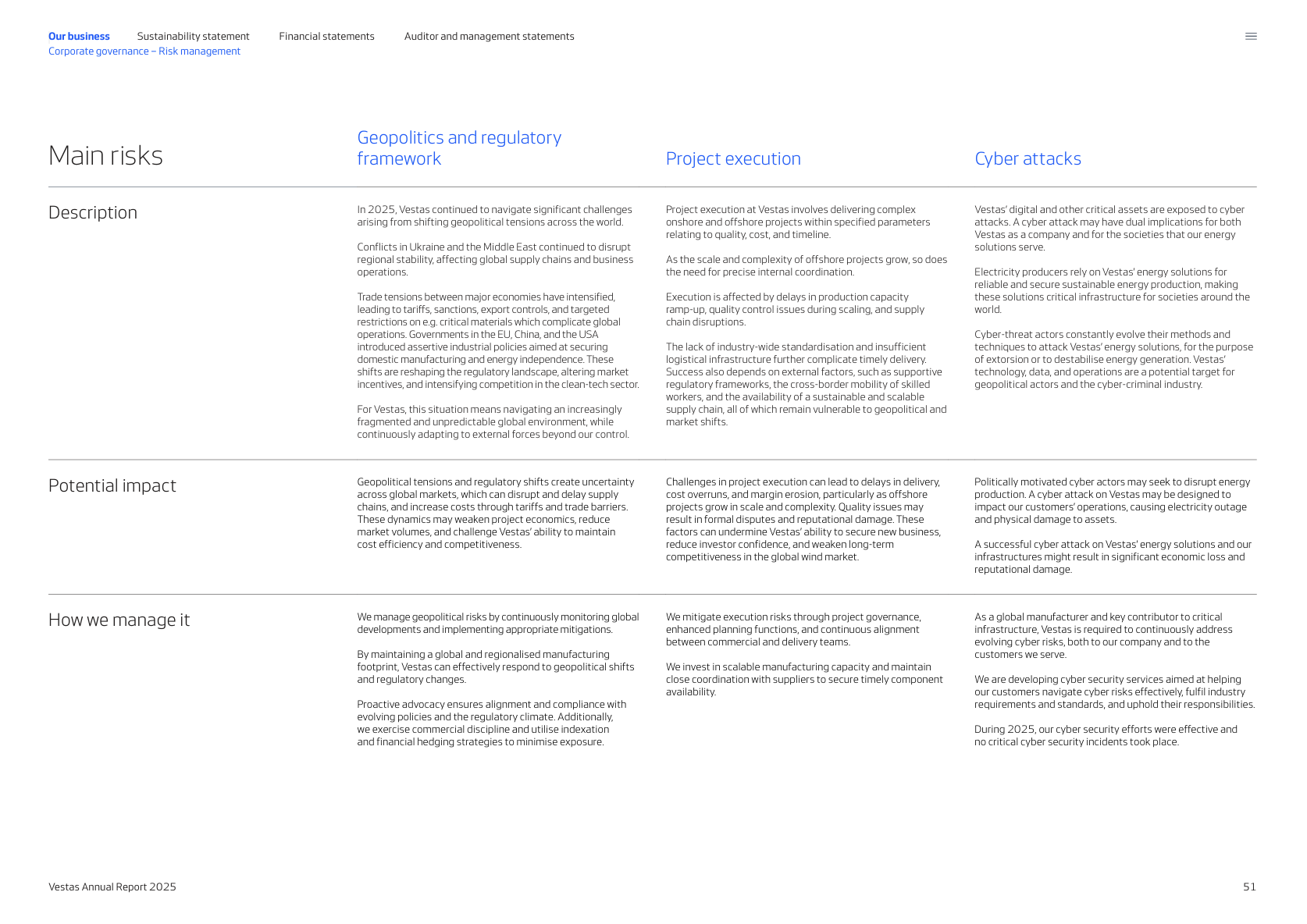

Novo Nordisk and Vestas redefine best practice ESRS reporting

The Novo Nordisk and Vestas FY2025 sustainability statements have redefined what best practice ESRS reporting looks like.

While most Wave 1 companies used their second year of CSRD reporting to refine their 2024 reports, Novo Nordisk and Vestas took a fundamentally different approach. They moved beyond compliance and built sustainability statements that are decision-useful, align more closely with the strategic and investor narrative, and clearly link to business value.

Both reports include innovations that raise the bar on what is possible. If you are benchmarking against a refined, compliance-focused report that builds incrementally on first-year CSRD reporting, you are looking in the wrong place.

For the forthcoming FY2026 reporting season, expect a widening gap between compliance-driven reports and those designed to inform investor decisions.

From volume to focus: what actually changed

The most visible change is the reduction in data points. The draft simplified ESRS removes all of the voluntary disclosures and cuts 61 percent of the mandatory set, resulting in an overall reduction of 71 percent in total data points. This is a significant adjustment in scope, but it does not fundamentally alter the intent of the framework.

The ambition remains to establish a strong reporting standard grounded in double materiality. What has changed is the level of granularity required to achieve that goal. In some areas, such as biodiversity, there are valid questions about whether ambition has been reduced. However, at a system level, the shift is better understood as a recalibration rather than a rollback.

The earlier version of ESRS was designed to be comprehensive, often leading companies to prioritize completeness over clarity. The revised version moves toward a more focused and proportionate model, where relevance becomes the guiding principle. This changes not only what companies report, but how they approach reporting as a whole.

The end of the 100-200 page ESRS report

One of the most visible changes is the reduction in size.

| Company | Word count (FY2025) | Reduction | Page Count (FY2025) | Reduction |

| Novo Nordisk | ~25,000 | -35% | 38 pages | -21% |

| Vestas | ~46,000 | -20% | 63 pages | -29% |

These are not marginal improvements. They show a deliberate shift from volume to clarity, where less content leads to stronger, more decision-useful reporting.

Many ESRS sustainability statements run to 100–200 pages or more, creating unnecessary complexity. Novo Nordisk and Vestas show this isn’t required: fully compliant sustainability statements can be delivered in 38 and 63 pages, respectively, excluding appendices.

In practice, this reflects a shift from treating the sustainability statement purely as a compliance document to functioning more like a management report while remaining fully compliant.

Novo Nordisk’s prioritized material topics

A defining feature of Novo Nordisk’s approach is the use of prioritized material topics to structure the report.

The underlying DMA still follows ESRS requirements to identify material impacts, risks, and opportunities. But on top of this, Novo Nordisk applies an additional layer of prioritization, focusing on topics that are 1) double material 2) score highest in the DMA, and 3) are clearly linked to strategic aspirations.

Rather than following the default ESRS order, the report is organized around what matters most to the business, leading with “Patient protection and quality of life” (S4) rather than defaulting to E1 Climate change.

This creates a clear narrative hierarchy and aligns the sustainability statement with strategic priorities. It represents a significant evolution in how the double materiality assessment (DMA) is used to shape the report.

In this sense, sustainability reporting is increasingly shaped by commercial dynamics rather than regulation alone. As a result, the conversation is shifting. Instead of focusing solely on compliance, companies are beginning to assess how reporting supports their broader positioning in value chains and financial markets.

The Vestas executive summary

While Novo Nordisk focused on restructuring the report, Vestas took a different path to the same objective.

Its most visible innovation is an 11-page executive summary that guides readers to the most important information. This includes key sustainability highlights, strategic priorities, and the results of the DMA.

This reflects a simple reality: not all users will read the full report.

By improving accessibility and navigation, Vestas ensures that key insights are visible and usable. This is particularly important for investors and senior decision-makers, who need to quickly understand material issues.

Together, these approaches show there is no single way to achieve decision-usefulness. What matters is the intent and execution.

Fewer actions, stronger evidence

One of the more counterintuitive changes is the reduction in the number of reported actions.

Both companies reduced their reported actions by around 20%, focusing only on those that drove the most impact.

This marks a shift from activity tracking to performance tracking. Instead of listing a wide range of initiatives, they applied clear filters: actions must be directly linked to material IROs, contribute to targets, and be measurable. Standalone initiatives were removed.

The result is a smaller set of actions that drive the most impact and are supported by verifiable evidence from subject matter experts, with clearer traceability for assurance.

Eliminating compliance-driven boilerplate,

Perhaps the most important shift is the change in language and narrative.

Both reports move away from ESRS-style phrasing and compliance-driven boilerplate, focusing on clearer, more decision-useful language.

Disclosures are written to guide the reader and emphasize what matters most, with a clearer link between material topics, impacts, risks and opportunities, and how they are managed.

Sustainability topics are more explicitly linked to strategy and priorities, and metrics are presented alongside targets and actions with clearer traceability.

The result is a narrative that reads like a management report: structured, analytical, and focused on what matters for decision-making. Sustainability is not positioned as a separate disclosure exercise, but as an integrated part of how the business is managed and evaluated.

Engaging auditors is critical

A key enabler of the innovations in the Novo Nordisk and Vestas reports is the approach to assurance.

Both companies engaged early and extensively with their auditors to enable changes in structure and content. This included detailed discussions, documentation, and compromises.

Their auditors required clear justification for the structural changes.

For example, Novo Nordisk was required to provide a clear DMA visual to clarify the prioritization and ordering of topics, along with additional navigational cues to help readers orient themselves despite the non-standard ESRS structure.

Vestas faced constraints in its executive summary: it could include only information already disclosed in the sustainability statement and had to present a balanced view, avoiding cherry-picked highlights.

This underlines a key point: innovation within ESRS is possible, but it requires strong governance, clear rationale, and close collaboration with auditors.

For FY2026, the assurance conversation will shape how many reports are designed and written.

Practical lessons for FY2026 reporting

Companies preparing for FY2026 should take note of several lessons from Novo Nordisk and Vestas:

- Apply a strict decision-usefulness filter. Challenge every voluntary disclosure: does this add value, is it decision-useful?

- Use the DMA to prioritize topics and drive the structure of the report

- Consider an executive summary to guide the reader to what matters

- Build a clear IRO → policy → action → target → metric chain with traceability

- Filter actions: include only those actions with the most impact that are tightly linked to material IROs and supported by evidence

- Remove repetition and ESRS-style boilerplate language

- Engage with your auditor early and extensively to move away from rigid, compliance-driven templates

Redefine your reporting objectives

Novo Nordisk and Vestas have set a new standard in ESRS reporting.

Both reports introduce innovations that go beyond incremental improvement and reset expectations for what a sustainability statement can deliver.

Looking ahead to FY2026, the question for every reporting team is: will your statement be a compliance document or a management report that drives business value?

It’s time to redefine your reporting objectives for FY2026 and that’s something we can help you with at Position Green.

Chat with us