How proactive sustainability teams are already preparing for 2027 reporting

There is a pattern in sustainability reporting that almost everyone recognizes and almost no one breaks. The reporting window closes. A brief recovery period follows. Then, somewhere around October, a familiar anxiety sets in: structures need revisiting, data gaps appear, organizational changes were never captured, and the external support you need is suddenly in high demand.

The crunch that follows is not bad luck. It is the predictable consequence of a decision made months earlier: to treat the post-season window as recovery time rather than preparation time.

This article is about breaking that pattern and why the case for doing so is stronger than most sustainability professionals realize.

Why the post-reporting window matters for 2027 readiness

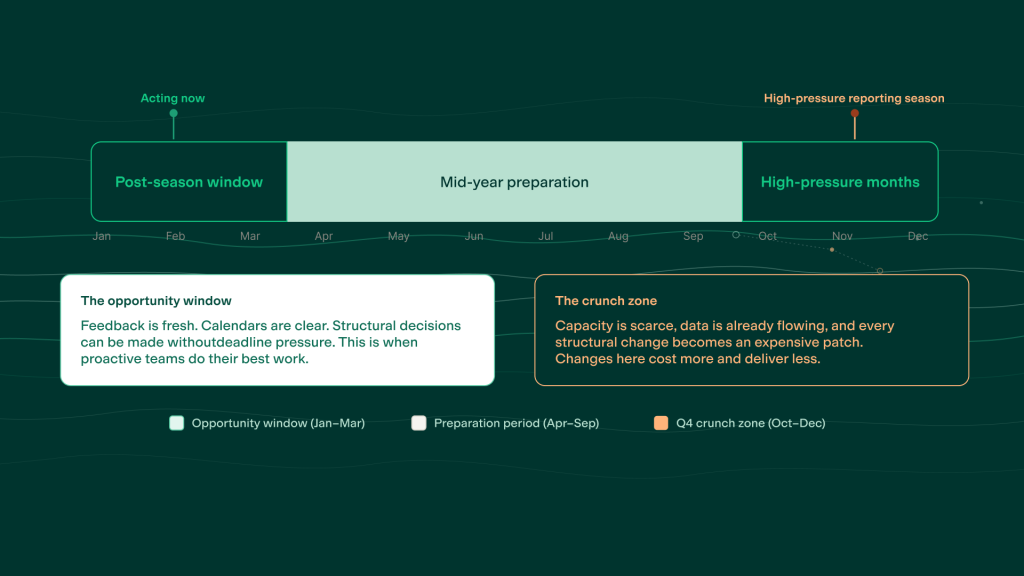

Reporting season has a short, structurally underused aftermath. Feedback from data reporters is still fresh. The frustrations , the metrics that were impossible to source, the organizational units that did not map cleanly, the definitions nobody could agree on , are live in people’s memories. In three months, they will not be.

This is the single best moment to run a structured debrief: what worked, what created bottlenecks, and what the data actually revealed once it was in. Not to relitigate the last cycle, but to convert that experience into a concrete plan of action before institutional memory fades.

It is also, critically, a moment of relative calm. The data work is done. There are no immediate deadlines forcing reactive decisions. That means structural choices can be made deliberately rather than under pressure, which consistently produces better outcomes, at lower cost, with less downstream maintenance.

Three steps to improve your sustainability reporting process before Q4

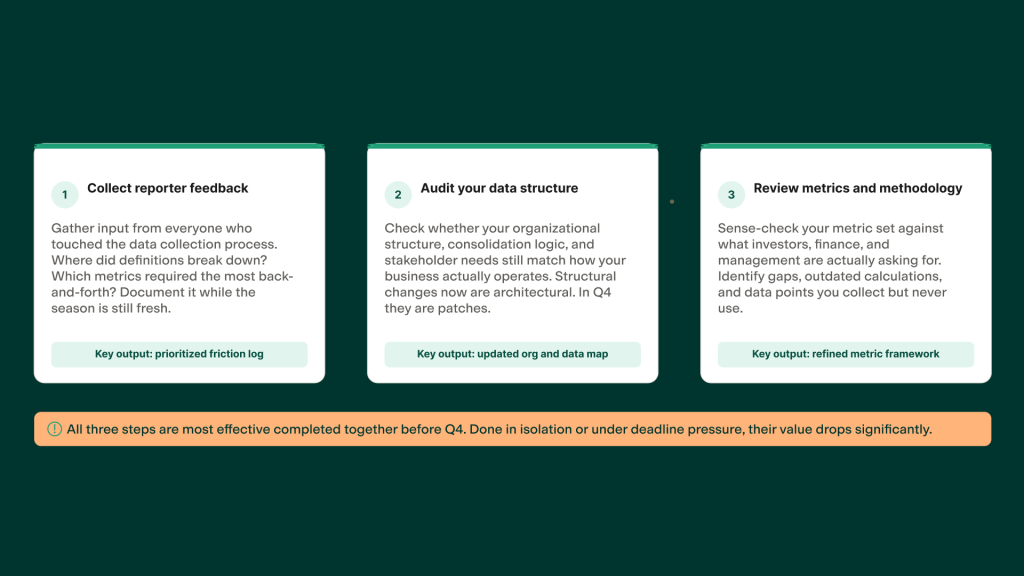

1. Collect and document feedback from your data reporters

The people who collected data for you have opinions about that process. They know where definitions were unclear, which metrics required three email threads to source, and which parts of the data collection felt designed for someone else’s organization rather than yours.

Common sticking points tend to cluster around the same areas year after year: energy and electricity data, where people struggle to find the right definitions or locate the figures at all; waste metrics, which often require manual reconciliation across multiple systems; and scope boundaries, where it is never entirely clear which sites or business units should be included.

Gathering this feedback now does two things. First, it identifies the friction points that quietly inflate reporting effort year after year. Second, it signals to your data owners that their experience of the process matters, which counts for more than it might seem when you need their cooperation again in Q4.

Document what comes back. Assign owners. Set a timeline for resolution. Done now, this is a structured improvement project. Done in November, it is a crisis.

2. Audit your data structure before the next collection cycle opens

Every organization changes. Business units are added, restructured, or divested. Subsidiaries change scope. New legal entities come into reporting boundaries. And every year, there are cases where the reporting structure built in Q4 reflects the organization as it was, not as it is.

Now is the time to check three things. First, your organizational structure: does it reflect the actual shape of your business going into 2027, including any changes expected before the reporting period opens? Second, your consolidation logic: how is data being rolled up, and are there units that were inadvertently excluded or included incorrectly? Third, your stakeholder requirements: have finance, HR, or investor relations signaled any new data needs that the current structure does not serve?

This last point is worth dwelling on. Sustainability data increasingly feeds decisions beyond the sustainability report itself: treasury teams use it for green financing, procurement uses it for supplier risk, and investor relations uses it for ESG ratings responses. A structure built purely for compliance may be leaving value on the table for the teams that need it most.

Restructuring data architecture is significantly harder once data is in the system. Changes made now, before the next collection cycle opens, are architectural. Changes made in November are expensive patches.

3. Review your metrics and methodology while context is still fresh

Custom calculations, conversion factors, and measurement methodologies accumulate over time. They are often built to solve an immediate problem, documented incompletely, and then inherited by whoever comes next. The people who made the original decisions may still be around. Ask them now.

This is also the moment to sense-check your metric set against evolving stakeholder expectations. Are investors or management asking for data points that your current setup does not surface cleanly? Are there metrics you collect but never use, or metrics you need but cannot currently produce without significant manual effort?

Aligning on this now means the 2027 reporting cycle can be designed to generate value, not just satisfy a filing requirement.

The risks of leaving 2027 reporting preparation until Q4

It is tempting to assume that waiting preserves optionality: that you will have a clearer picture of requirements later in the year, and that acting early means acting on incomplete information. In practice, the opposite tends to be true.

Something will always come up in November or December. An organizational change. A new regulatory clarification. A stakeholder request that was not anticipated. This is not a reason to delay preparation. It is a reason to have a solid foundation in place so that late-breaking changes can be absorbed without destabilizing the whole process.

The specific risks of late preparation tend to cluster around three areas:

Data integrity. Retroactively restructuring reporting frameworks once data has started flowing is significantly more complex than building the right structure upfront. Errors introduced under time pressure are harder to audit and correct.

Capacity constraints. External advisors, platform providers, and internal specialists are all under peak demand in Q4. Organisations that start late often find that the support they need is either unavailable or comes at a premium.

Strategic shallowness. When everything is built to meet a deadline, there is no room to ask whether it could also serve a broader purpose. The result is a compliance artifact rather than a decision-making tool, which then generates its own feedback loop of dissatisfied stakeholders and demands for additional reporting.

How early preparation unlocks strategic value beyond compliance

There is a version of this work that is purely about operational readiness: fixing the friction points, updating the structure, cleaning up the methodology. That version is valuable and worth doing.

But there is a more ambitious version, and the post-season window is the only time in the calendar when it is genuinely accessible.

That version starts with a different set of questions. Not what do we need to report, but what does our data tell us that we have not yet acted on? Not how do we meet the requirement, but what would investors, management, or the board actually find useful to see, and can we build toward that now?

Sustainability data has a latent value that most organizations never fully unlock, because the process of generating it consumes all available energy. The professionals who get ahead of their reporting cycles are the ones who find time to ask the more interesting questions: where are our biggest operational inefficiencies? Which supplier relationships carry the most material risk? What would it take to credibly link our sustainability performance to our cost of capital?

Those conversations require time, data, and bandwidth. All three are available right now. In November, none of them are.

Building a sustainability reporting process designed to last

There is a dimension to this that rarely makes it into process documentation but is worth naming directly. Sustainability reporting done under sustained time pressure is exhausting: for the professionals running it, for the data owners contributing to it, and for the external partners supporting it.

The irony is not lost on sustainability professionals that a function dedicated to long-term resilience so frequently operates in a mode of short-term crisis management. Building a process designed for longevity, one that distributes effort evenly across the calendar rather than compressing it into six weeks, is itself an act of sustainable practice.

It also tends to produce better work. Decisions made under pressure are optimized for speed, not quality. A reporting process built with adequate time for reflection, stakeholder input, and internal quality assurance is more likely to hold up under audit, generate useful insight, and serve the organization beyond a single reporting cycle.

Where to start your 2027 reporting preparation

If you are reading this in the weeks following your last reporting submission, the most useful thing you can do today is block time for a structured retrospective before the memory of the season fades. Bring in your data owners, your internal stakeholders, and anyone who had visibility of the process end to end.

From that conversation, three things should emerge: a prioritized list of structural improvements, a clear picture of what your key stakeholders actually need from your 2027 data, and an honest assessment of where your current setup does and does not serve those needs.

That is your plan of action. The window to execute it well is open now, so do not miss the chance to capitalize on it.

Position Green helps organizations build and maintain sustainability reporting processes that are audit-ready, stakeholder-aligned, and designed to generate insight beyond compliance. To explore how we support your 2027 reporting readiness, get in touch with our team.

Chat with us

Sanjidul Huda

Senior Customer Success Manager

Position Green