Unpacking the EBA Guidelines: What’s changing and why it matters

With application beginning in January 2026 for most institutions, ESG risk is now embedded in supervisory expectations governing strategy, risk management, and capital planning.

Importantly, this development is not primarily about sustainability reporting. It is about how banks understand, govern, and price risk.

From sustainability narrative to prudential expectation

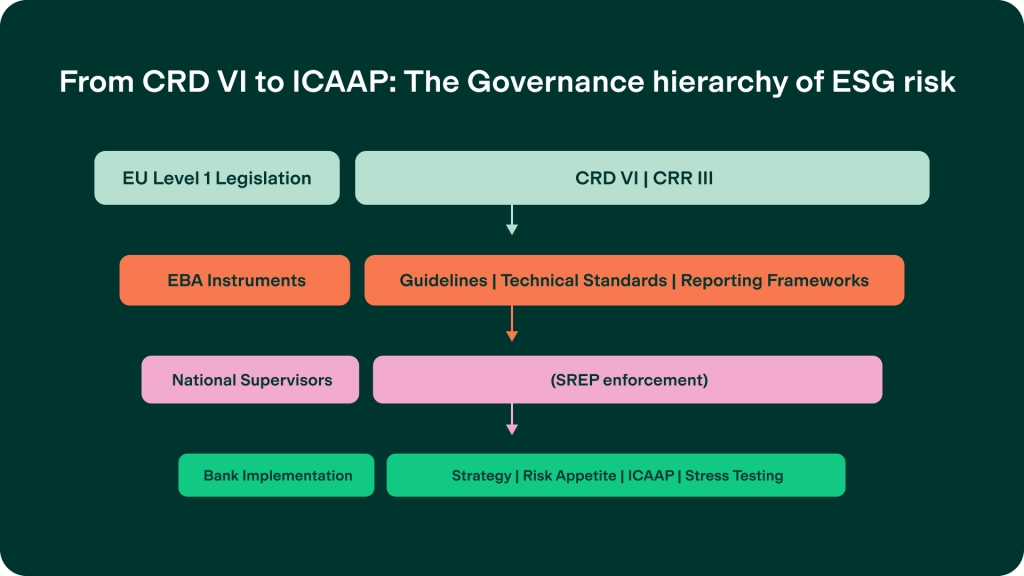

The EBA shapes the European banking framework through multiple regulatory tools. Technical standards define binding requirements. Reporting frameworks determine what institutions must disclose. The ESG risk management guidelines sit in a different category: they establish supervisory expectations for how banks must integrate ESG risks into existing risk frameworks.

These guidelines are assessed and enforced through national supervisory authorities as part of the Supervisory Review and Evaluation Process (SREP). In practice, this means supervisors will evaluate whether ESG risks are credibly embedded in governance structures and risk processes.

The shift is conceptual as much as operational. ESG risk is not treated as a standalone category. It must be mapped into traditional prudential risk types; credit, market, operational, liquidity, and reputational risk and managed accordingly. This integration is what fundamentally changes the conversation.

Risk appetite: explicit rather than implicit

One of the most consequential elements of the guidelines concerns risk appetite.

The EBA does not prohibit banks from taking on ESG-related risk. Institutions remain free to define their own strategic positioning and sectoral exposure. What changes is that ESG risk can no longer remain implicit.

Banks are expected to articulate how ESG risks fit within their risk appetite framework. This includes defining tolerance levels, monitoring exposures, and ensuring board-level oversight.

In practical terms, this means a bank financing carbon-intensive sectors must demonstrate that it understands the associated transition risks, has assessed the potential financial impact, and has aligned those exposures with its declared risk appetite.

The EBA does not prohibit banks from taking on ESG-related risk. Institutions remain free to define their own strategic positioning and sectoral exposure. What changes is that ESG risk can no longer remain implicit.

“Banks now need to explicitly take into consideration how sustainability-related risks could affect a company’s operations and financial performance over time.”

Tony Christensen, Chief Sustainability Officer, Norion Bank

Banks are expected to articulate how ESG risks fit within their risk appetite framework. This includes defining tolerance levels, monitoring exposures, and ensuring board-level oversight. In practical terms, this means a bank financing carbon-intensive sectors must demonstrate that it understands the associated transition risks, has assessed the potential financial impact, and has aligned those exposures with its declared risk appetite.

While this approach builds on established risk management principles familiar from traditional financial risk frameworks, the application of ESG risk introduces new complexities. Unlike conventional risks, ESG factors are inherently forward-looking, systemic, and often characterised by long time horizons and limited historical data. As a result, the methodologies used to assess, monitor, and manage these risks must evolve accordingly.

Rather than a simple extension of existing practices, integrating ESG into risk management requires adapting each step of the process to account for uncertainty, scenario-based thinking, and the transformative nature of sustainability-related risks.

Materiality and transmission channels

The guidelines require regular ESG risk materiality assessments. These assessments are not abstract exercises. They must identify how environmental, social, and governance factors translate into financial risks over different time horizons.

For example, climate transition risk may affect borrower profitability and creditworthiness. Physical risk may influence collateral valuations. Governance weaknesses may heighten counterparty risk. Social controversies can affect operational continuity.

The expectation is that institutions move beyond high-level ESG categorization and instead identify the transmission channels through which ESG factors impact balance sheet risk.

For larger institutions, these assessments must be conducted at least annually, and the results must inform both strategy and risk management decisions.

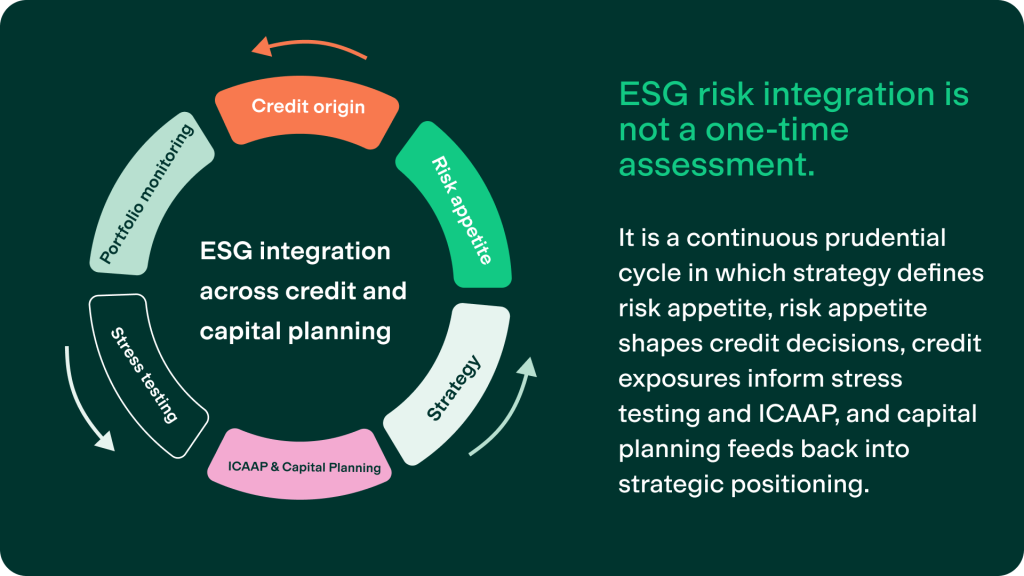

Integration into credit processes and capital planning

The most substantive operational change lies in how ESG risk is integrated into core prudential processes.

Loan origination frameworks must reflect ESG risk considerations. Ongoing credit monitoring must incorporate forward-looking risk indicators. Portfolio analysis must account for sectoral and geographic ESG exposures. Scenario analysis and stress testing must consider long-term transition and physical risk pathways.

Most significantly, ESG risks must be reflected within the Internal Capital Adequacy Assessment Process (ICAAP). This moves ESG from a disclosure topic to a capital planning consideration.

Supervisors will examine whether institutions have credible methodologies for identifying and quantifying ESG risks, whether those risks are incorporated into capital assessments, and whether governance structures ensure effective oversight.

Transition planning as a supervisory expectation

Another forward-looking requirement concerns transition planning. Institutions must prepare plans outlining how they manage financial risks arising from the transition to a more sustainable economy.

These plans are not simply climate pledges. They are risk management tools. They should contain measurable objectives, timelines, governance arrangements, and portfolio considerations aligned with the institution’s strategic positioning and risk appetite.

Supervisors will evaluate whether transition plans are coherent, internally consistent, and supported by credible analysis.

Again, the focus is not ambition. It is prudential resilience.

Interaction with CRD, CRR and reporting frameworks

The ESG risk management guidelines sit within a broader regulatory architecture.

CRD VI provides the legal basis for integrating ESG risks into supervisory review. CRR III and associated Pillar 3 requirements define disclosure obligations. Reporting frameworks determine what data must be collected and reported.

The guidelines connect these elements. They translate legislative intent into operational expectations for governance and risk management. While data collection remains important, data is a means to support risk integration rather than the primary objective.

Why this matters beyond banks

Although the guidelines apply directly to financial institutions, their implications extend to corporate borrowers.

If banks must integrate ESG risks into credit assessments, stress testing, and capital planning, they must also evaluate how counterparties are exposed to environmental and social risk drivers. Companies seeking financing can therefore expect greater scrutiny of transition exposure, physical risk vulnerability, governance quality, and long-term strategy.

The EBA guidelines shape how banks evaluate risk. In doing so, they indirectly shape how companies are assessed in lending decisions.

“For companies, this is less about additional reporting and more about demonstrating a clear understanding of their risk exposure and how they plan to manage it.”

Tony Christensen, Chief Sustainability Officer, Norion Bank

A structural recalibration

The EBA has not introduced new sustainability obligations in isolation. It has embedded ESG risk within the prudential core of banking supervision.

Institutions remain free to define their own business models and sector exposures. What has changed is the expectation that ESG risk must be systematically identified, explicitly governed, integrated into capital planning, and aligned with risk appetite.

In 2026, ESG risk management is no longer a discretionary narrative. It is prudential infrastructure.

And that fundamentally changes how risk is understood across the financial system and, by extension, how you should view risk yourself. Most businesses don’t understand the extra-dimensionalities of their risk exposure that are uncovered by sustainability due diligence. But right now you can model it yourself using our free ROI calculator tool.

You will be able to see not only the financial upsides of enabling core sustainability initiatives across your organization, but how not taking action on them can also lead to loss of revenue and unexpected exposure year on year.

See ROI calculator

Tony Christensen

Chief Sustainability Officer

Norion Bank