Answers from auditors: common ESRS challenges and how to solve them

The key question is no longer just what you disclose, but whether your disclosures are reproducible, complete, and clearly connected.

In a recent live session with ESRS auditors, we reviewed a report in real time and discussed common challenges faced during first-time reporting. A consistent theme emerged: most audit issues are not caused by missing disclosures, but by gaps in structure, traceability, and internal logic.

Audit-ready reporting is reproducible

A well-written report is not enough. Audit readiness depends on whether:

- Disclosures can be reproduced

- Data is complete

- Information is connected across the report

This means reporting must be built on consistent processes. If datapoints cannot be traced back to their source, or if the same inputs do not lead to the same outputs, the report will not hold under audit.

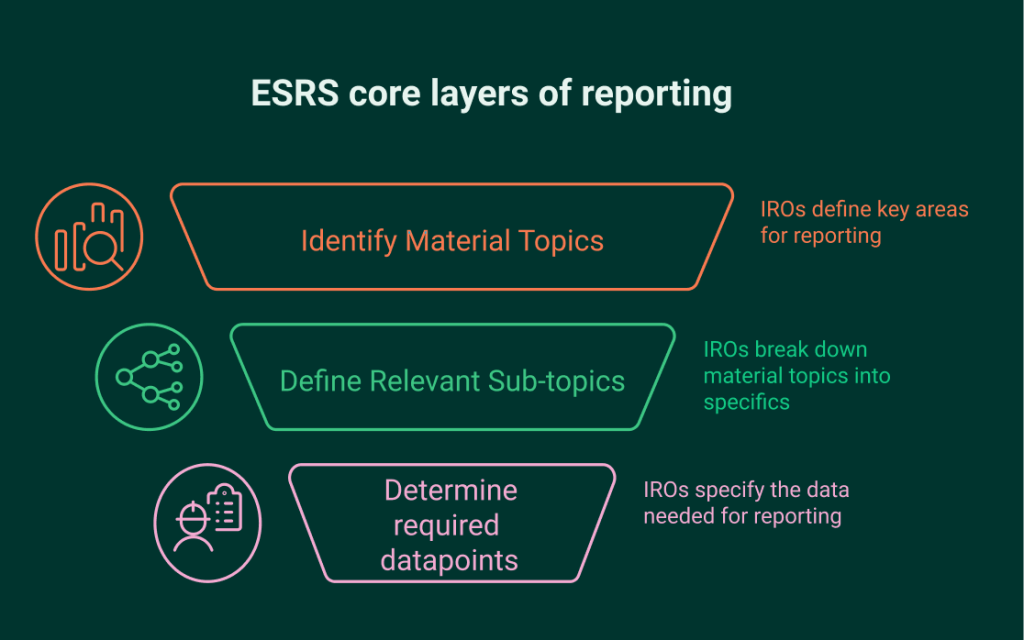

IROs drive the entire report

ESRS follows a clear logic: impacts, risks, and opportunities (IROs) determine what should be disclosed. IROs define:

- Material topics

- Relevant sub-topics

- Required datapoints

A common mistake is starting with ESRS topics and mapping IROs afterward. This often leads to inconsistencies and gaps. Strong reports maintain a clear link between IROs and all disclosures.

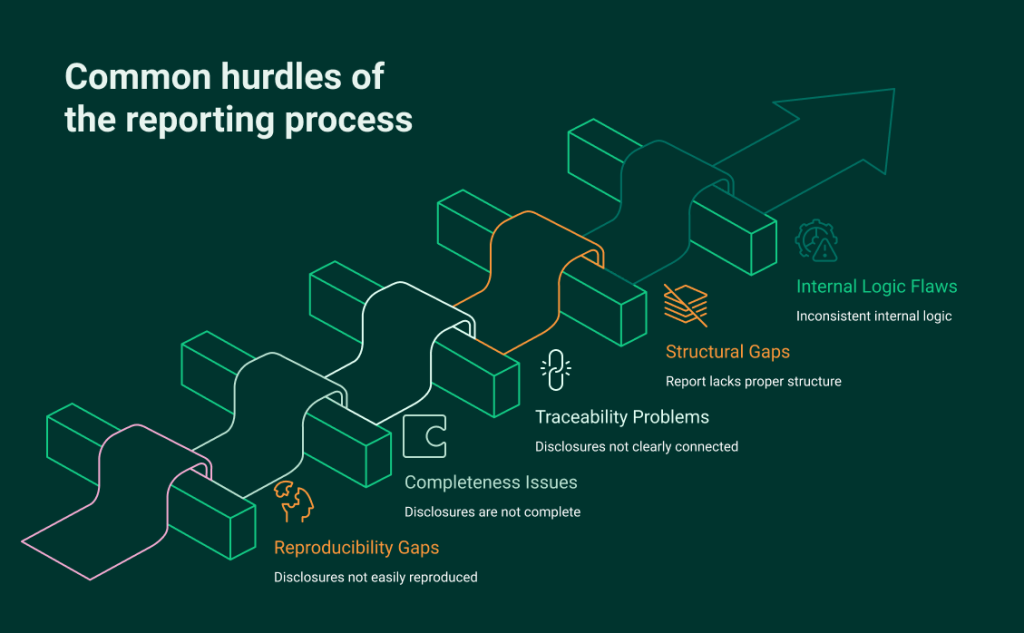

Where reports typically break down

Most reports include the right elements. The challenge is how they connect.

Common issues include:

- Weak links between IROs and disclosures

- Policies not tied to material topics

- Metrics without clear methodology or context

- Inconsistencies between sections

These issues often only become visible during audit.

Common audit challenges

Across first-time reporters, several patterns stand out:

Incomplete value chain coverage

Risks and impacts are not fully assessed across the value chain

Missing datapoint materiality

Materiality is assessed at topic level, but not extended to datapoints

Weak topic–IRO linkage

Disclosures are not clearly tied back to identified IROs

Limited connection to financial reporting

Sustainability disclosures are not aligned with financial data

Unclear definitions and time horizons

Impacts are not consistently defined or contextualized

Policies must reflect practice

Policies should not be high-level statements. They need to:

- Link directly to material IROs

- Align with actions and targets

- Show how risks and impacts are managed in practice

Without this, they are difficult to validate during audit.

Materiality must be applied consistently

Materiality is not a one-time exercise. It should guide the entire report.

Auditors assess whether:

- Topics reflect the DMA outcome

- Datapoints align with those topics

- Disclosures are consistent across sections

Stopping at topic-level materiality often creates gaps.

Handling data gaps

Data gaps are expected, especially in early reporting cycles. What matters is transparency.

Organizations should:

Apply consistent methods over time

Explain methodologies and assumptions

Document estimation approaches

Traceability depends on governance

Traceability requires more than systems. It depends on governance.

Strong reporting typically includes:

- Clear ownership of datapoints

- Documented methodologies

- Internal review processes

- Defined data controls

Key misconceptions to avoid

Several misconceptions continue to create challenges:

- Double materiality is not a one-off exercise

- Sustainability reporting is not separate from financial reporting

- Limited assurance still involves structured testing

- Audit scope goes beyond metrics to include processes and governance

What this means in practice

Audit readiness depends on structure, not just presentation.

Organizations that succeed typically have:

- Clear ownership and accountability

- Consistent application of materiality

- Strong links between IROs, policies, actions, and metrics

- Traceable and well-documented data

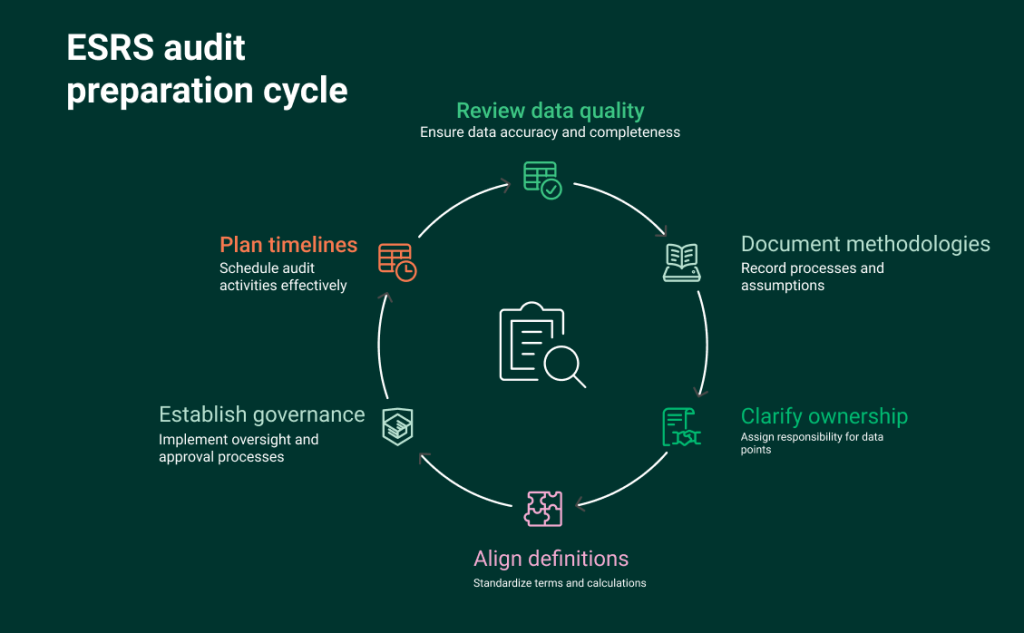

How to prepare for ESRS audit

There is no single best method for preparing for ESRS audit that works across the board for businesses. But solid practical steps include:

- Plan timelines for the audit process

- Review data quality before audit

- Document methodologies and assumptions

- Clarify ownership of key datapoints

- Align definitions and calculation methods

- Establish governance and sign-off processes

What makes this infinitely easier though is working within a software built to make the collaboration between you and auditors easy and less resource-intensive. Our customers routinely save time and reduce both their internal and external workloads, lending them more time to capitalize on the strategic value of their data, while excelling in their reporting.

Learn more about Position Green