6 reasons why a sustainability business case breaks down

The numbers, in isolation, are usually defensible. What breaks the case is almost never the math. It’s the organizational and structural context the math has to survive once it leaves the model and enters a real capital allocation process, a real reporting line, and a real earnings call. Below are six of the most consistently documented reasons a sound sustainability business case still collapses in practice.

Position Green recently hosted a webinar on the guidelines with Maria Hållvik Stensland, senior manager and head of sustainable finance at Position Green, and Tony Christensen, Chief Sustainability Officer at Norion Bank. What follows are the key takeaways, aimed as much at the businesses being financed as the banks doing the financing.

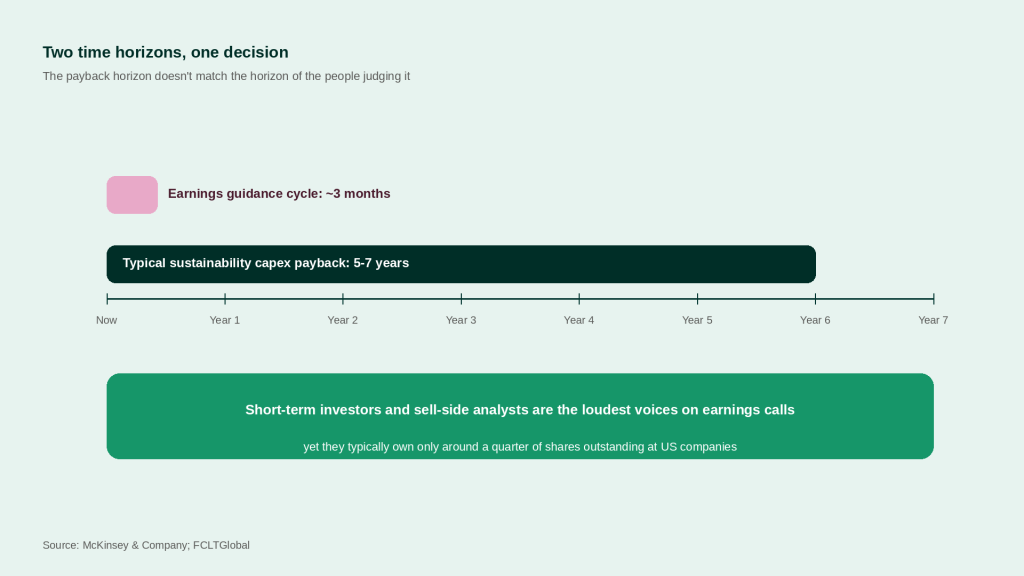

The payback horizon doesn’t match the horizon of the people judging it

Companies that issue quarterly guidance train their leadership to protect next quarter’s number, and when earnings look like they’ll miss the promised range, the documented pattern is that leaders adjust revenue or costs to hit it anyway rather than let the miss stand. Sustainability capex typically carries a longer, less certain payback profile than a standard growth project, so in any capital-rationing conversation it reads as the item you can defer without an immediate P&L consequence.

This happens despite the fact that short-term investors and sell-side analysts, who are the most visible voices on earnings calls, typically own only around a quarter of shares outstanding at US companies. The case doesn’t fail on its economics. It fails because the loudest evaluators in the room are structurally biased toward a shorter time horizon than the investment operates on.

Nobody owns it, so it has no defender when budgets get cut

A recurring pattern across the organizational-barriers research is that sustainability initiatives stall specifically where accountability is diffuse.

When no individual or function is explicitly on the hook for an outcome, the initiative has no natural advocate in the room where trade-offs actually get made, which makes it the first thing cut under resource pressure.

A review of more than 50 corporate sustainability programs found the same failure from the practitioner side: programs lose momentum when there’s no execution plan with named initiatives, roles, and deadlines attached, and separately, when the team can’t frame the work as serving core business objectives like revenue or risk reduction rather than as a parallel agenda running alongside the real business.

The leadership signal doesn’t survive the trip down the org chart

Research on this distinguishes between leadership that’s genuinely absent and leadership that’s merely ambiguous, and the ambiguous case is the more common and more damaging one.

External communications about sustainability commitments are often strong, while internal signals to middle managers are weak or contradictory, so middle managers reasonably interpret that gap as meaning their own day-to-day behavior should follow internal norms, not external commitments, and that sustainability isn’t actually expected of them personally.

A related study of a sustainability-oriented innovation strategy found the same breakdown even where top management commitment was genuine: middle managers and frontline staff were still unclear on what actually constituted the business case for the initiative. The case can be entirely sound at the top and still die on the way down, because “sustainability matters” was never translated into what a specific manager should do differently in a specific trade-off.

The practical challenges cluster around four The investment gets measured with the wrong ruler

Sustainability investments typically carry a different risk-return profile and more uncertainty than a standard capex request, and organizations that handle this well have generally set aside a dedicated funding pool, defined separate hurdle rates, or in some cases introduced an internal carbon price to make the comparison fair.

Absent that adjustment, a sustainability project gets run through the same IRR hurdle as a factory expansion and loses, not because it’s a worse investment, but because it’s being measured with a ruler built for something else.

This connects to what’s sometimes called the black box problem: companies routinely commit substantial management time and capital to sustainability activity while rarely quantifying, in the same rigorous NPV terms they’d apply to any other investment, what returns it generates or what value is actually at stake. If the number was never rigorously shown in the first place, it can’t be defended later when someone else needs the budget.

Regulatory volatility keeps reopening a case that was supposedly closed

This one is unfolding in real time rather than sitting in a historical case study. Companies spent 2023 to 2025 building compliance-anchored business cases around CSRD timelines. The EU’s Omnibus I package, finalized in February 2026, then raised the CSRD turnover threshold from €150 million to €450 million and pushed reporting for Wave 2 and 3 companies from 2026 to 2027, removing roughly 42,000 companies from scope entirely.

For any internal case that leaned on “the deadline forces this,” the deadline moving is functionally the same as the ROI moving. Legal analysis of the directive is explicit that this isn’t a retreat in substance, thresholds rose and timelines extended, but the underlying obligations were recalibrated rather than withdrawn, and the package includes a scope review clause that could tighten requirements again later.

That nuance rarely survives inside a company once “the mandate went away” becomes the internal narrative, which is exactly why cases built primarily on regulatory compulsion tend to be more fragile than cases built on the underlying financial exposure the regulation was only ever pointing at.

The underlying strategic logic has genuine, unresolved skeptics in the academic literature, not just in the C-suite

This is worth knowing because it explains why some of the resistance a business case runs into isn’t ignorance, it’s a legitimate open question. Research in the sustainability strategy literature has argued that the shared-value business case for sustainability faces the same organizational resistance that blocks disruptive innovation generally, drawing directly on Bower and Christensen’s classic account of why established firms struggle to invest in disruptive technology, and arguing the two blocking processes are structurally similar. The implication is uncomfortable but useful: even a well-built sustainability business case competes for exactly the same scarce management attention and resourcing pathways that already reliably kill disruptive-but-unproven investments of any kind. Sustainability isn’t specially vulnerable because it’s sustainability. It’s vulnerable for the same structural reasons any long-payback, uncertain-return investment is vulnerable inside a large organization.

None of these six failure modes are really about whether the underlying investment makes financial sense. They’re about time horizon mismatch, diffuse ownership, signal loss between leadership and the people executing, measurement tools built for a different kind of investment, a regulatory floor that keeps moving, and a resourcing competition every long-payback investment faces regardless of subject matter. A business case that anticipates these six failure points before it’s built survives contact with a real budget cycle. One that doesn’t, however sound its economics, generally doesn’t.

Ready to make the business case durable, not just correct

A sound business case doesn’t stay sound on its own. Ownership changes hands, budget cycles reset, and without a system that keeps the original logic visible, the same six failure points tend to reassert themselves within a year or two.

Position Green’s software services team implements the infrastructure that keeps a business case alive after it’s approved: named-owner accountability built into the workflow, NPV and hurdle-rate tracking that holds sustainability investment to the same rigor as any other capital request, and monitoring that surfaces early when a case is drifting back toward being read as a parallel agenda rather than a core one. We implement this at scale for your team, so the fix outlives the person who built it.

Explore our software services