EFRAG reveals first details of the N-ESRS: What non-EU companies need to know after Omnibus

First, the Omnibus reforms have dramatically reduced the number of companies expected to fall within scope, from around 10,000 to approximately 1,200 according to EFRAG’s preliminary estimates.

Second, despite this reduction in scope, the N-ESRS remains a substantial reporting framework covering governance, strategy, policies, actions, metrics and targets across twelve standards.

For non-EU companies that remain within scope of Article 40a of the Accounting Directive, the latest proposals provide the clearest indication yet of future reporting requirements and the likely direction of travel for sustainability reporting in Europe.

The largest share of affected companies is expected to be headquartered in the United States, followed by the United Kingdom, Switzerland and Japan.

What is N-ESRS and why was it created?

The N-ESRS has been several years in the making.

The legal foundation was established in April 2021 when the European Commission proposed the CSRD. From the outset, the proposal included a requirement for certain non-EU companies with significant activity in the European Union to disclose sustainability information at group level.

When the CSRD entered into force in December 2022, the requirement for non-EU reporting was retained in Article 40a of the Accounting Directive.

Article 40a is the provision of the Accounting Directive that requires certain non-EU groups with significant EU activity to publish sustainability information at group level.

The legislation also mandated the development of dedicated sustainability reporting standards for non-EU groups.

EFRAG subsequently began technical work on the standards and published initial working drafts during 2024, providing the first indication of how reporting requirements for non-EU companies might differ from the European Sustainability Reporting Standards (ESRS) applicable to EU undertakings.

However, the Omnibus reforms fundamentally changed the landscape.

While Omnibus did not remove Article 40a or the requirement for dedicated non-EU sustainability reporting standards, it significantly reduced the number of companies expected to fall within scope. At the same time, EFRAG shifted much of its attention towards simplifying the ESRS for EU companies.

Following completion of its technical advice on the revised ESRS, EFRAG resumed work on the N-ESRS during 2026.

The June 2026 proposals therefore represent the first detailed public indication of the future direction of the N-ESRS since the Omnibus reforms reshaped the scope of CSRD reporting.

EFRAG currently plans to launch a public consultation in July 2026, deliver technical advice to the European Commission in January 2027 and support adoption of the final standard during 2027.

How Omnibus changed the scope of N-ESRS reporting

One of the most significant consequences of the Omnibus reforms was the dramatic reduction in the number of non-EU companies expected to report under the CSRD.

Pre-Omnibus thresholds

Before Omnibus, a non-EU group generally fell within scope if:

- The group generated more than €150 million of turnover in the EU at group level; and

- It had either an EU subsidiary or an EU branch generating more than €40 million in turnover.

Importantly, employee numbers were not considered when determining whether a non-EU company fell within scope.

Post-Omnibus thresholds for N-ESRS

The Omnibus reforms introduced substantially higher thresholds.

Non-EU companies will fall within scope of the N-ESRS for FY2028 reporting if they meet both of the following requirements:

- The non-EU parent company generates more than €450 million of net turnover in the EU for two consecutive years; and

- Has an EU subsidiary or branch generating more than €200 million in net turnover in the preceding financial year.

In other words, the €450 million EU parent turnover threshold must be met alongside a European presence through the additional subsidiary or branch criteria.

The reduction in scope is primarily driven by the increase in the EU turnover threshold from €150 million to €450 million, together with more restrictive subsidiary and branch criteria.

How many non-EU companies remain in scope?

According to EFRAG’s preliminary estimates, the revised thresholds reduce the number of companies in scope of the N-ESRS from approximately 10,000 to around 1,200.

The United States accounts for the largest share of companies expected to remain in scope, with an estimated 350-450 companies. The United Kingdom follows with approximately 150-200 companies, while Switzerland and Japan each account for around 100-150 companies.

Although the scope reduction is significant, the companies that remain in scope are predominantly large multinational groups with substantial operations and revenues connected to the European market.

As a result, N-ESRS reporting is expected to remain a significant sustainability reporting requirement for many of the world’s largest non-EU companies.

How does N-ESRS differ from ESRS?

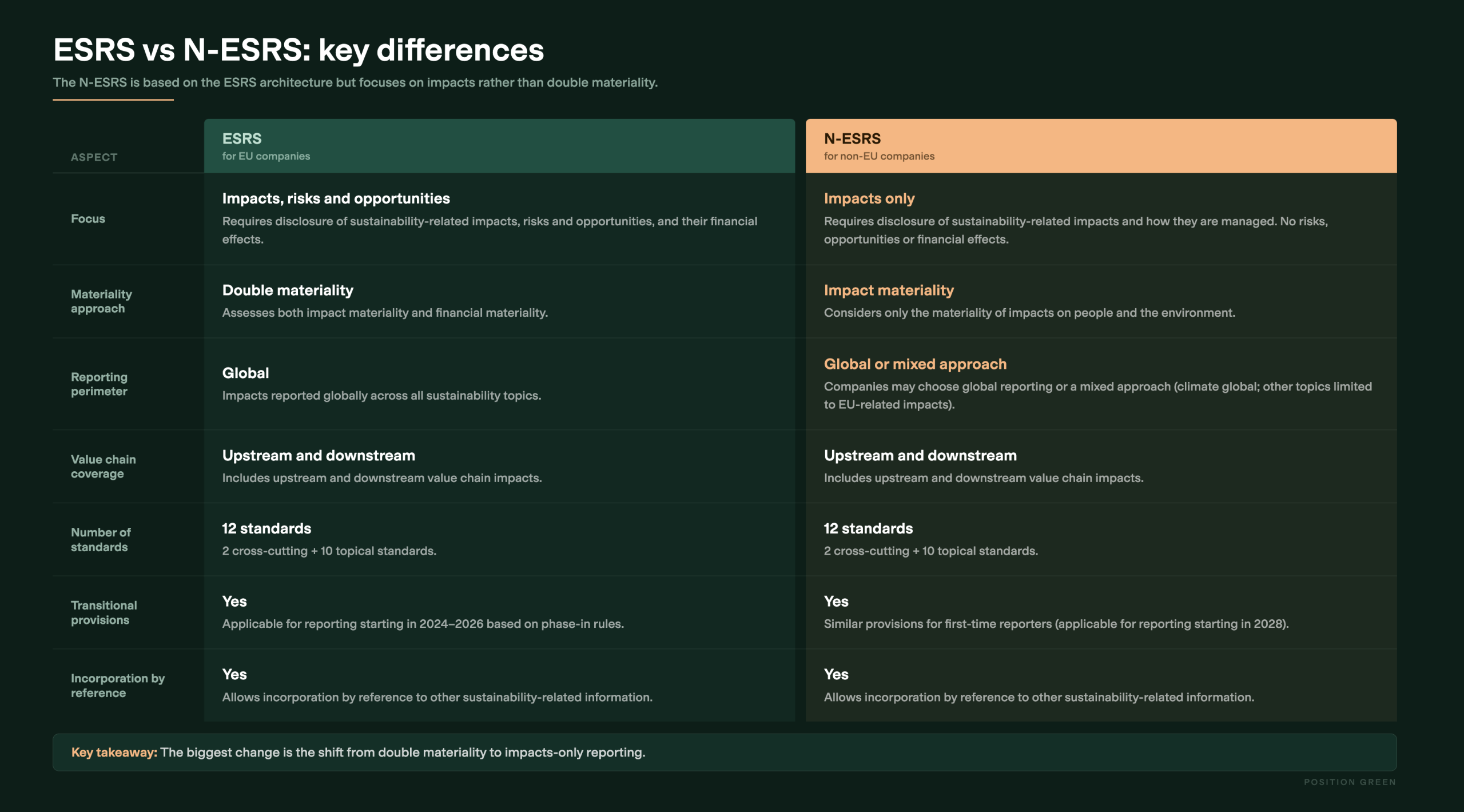

Perhaps the most significant feature of the proposed N-ESRS is its focus solely on impacts rather than on double materiality.

Unlike the ESRS applicable to EU undertakings, the N-ESRS would not require companies to report sustainability-related risks and opportunities or the financial effects arising from sustainability matters.

Instead, the proposed framework concentrates on the actual and potential impacts that companies have on people and the environment.

EFRAG’s drafting approach is based on the simplified ESRS currently under development but removes key financial materiality concepts, including:

- Risks and opportunities

- Financial effects

- Resilience of the business model and strategy

- Dependencies on sustainability matters

This reflects the original objective of Article 40a, which focuses on accountability and transparency regarding the impacts of non-EU companies operating in the European market.

However, companies should not assume that the reporting burden will be minimal.

The proposed framework still requires extensive disclosures across governance, strategy, policies, actions, metrics and targets.

What is the objective of the N-ESRS sustainability report?

While the N-ESRS focuses on impacts rather than double materiality, EFRAG has made clear that the overall objective of the sustainability report remains fair presentation.

The objective of the sustainability report, taken as a whole, is to present fairly the undertaking’s material sustainability-related impacts and how those impacts are managed.

This is significant because it establishes the overarching objective against which the individual disclosure requirements should be understood.

In practice, companies will need to provide a balanced and complete picture of their material impacts and the governance, strategy, policies, actions, metrics and targets used to manage them.

EFRAG also proposes to retain the same definition of users as under the ESRS. This includes both primary users of general-purpose financial reports and other users of general-purpose sustainability reports.

As a result, companies should not view the N-ESRS as a narrow compliance exercise. Even though the framework excludes risks and opportunities, financial effects, resilience and dependencies, the sustainability report must still provide decision-useful information that enables users to understand the company’s material impacts and how they are being managed.

The emphasis on fair presentation also helps explain why the N-ESRS continues to require extensive disclosures across governance, strategy, policies, actions, metrics and targets despite adopting an impacts-only approach.

What does N-ESRS require companies to report?

The proposed architecture mirrors the ESRS structure and consists of twelve standards based on the ESRS:

- N-ESRS 1 General Requirements

- N-ESRS 2 General Disclosures

- N-ESRS E1 Climate Change

- N-ESRS E2 Pollution

- N-ESRS E3 Water

- N-ESRS E4 Biodiversity and Ecosystems

- N-ESRS E5 Resource Use and Circular Economy

- N-ESRS S1 Own Operations

- N-ESRS S2 Workers in the Value Chain

- N-ESRS S3 Affected Communities

- N-ESRS S4 Consumers and End-users

- N-ESRS G1 Business Conduct

The reporting areas broadly align with the ESRS and cover:

- Governance

- Strategy

- Impact management through policies and actions

- Metrics and targets

In practice, companies should expect disclosures relating to sustainability governance structures, strategy, impact management processes, policies, actions, targets and performance metrics across environmental, social and governance topics.

Although the N-ESRS removes double materiality, it remains a comprehensive sustainability reporting framework rather than a limited disclosure regime.

The three reporting options under N-ESRS

One of the most important design choices currently being considered concerns the reporting perimeter.

EFRAG has proposed three possible approaches for companies reporting under Article 40a.

Option 1: Global reporting

Companies would report impacts globally across all sustainability topics.

This approach most closely resembles the reporting perimeter currently applied under the ESRS and would provide users with a complete picture of the undertaking’s sustainability-related impacts across its global operations and value chain.

Option 2: Mixed approach

Climate-related disclosures would be reported globally, while other sustainability topics could be limited to impacts that are considered EU-related.

Under the current proposal, EU-related impacts would include both:

- Impacts arising from products and services sold within the EU market

- Impacts arising from the company’s activities within the EU

This approach is intended to reduce reporting complexity while maintaining transparency regarding impacts connected to European operations and markets.

Option 3: Voluntary application of full ESRS

Non-EU parent companies could voluntarily apply the full ESRS instead of the N-ESRS.

This option may be particularly attractive for multinational groups with significant EU operations because it could allow certain EU subsidiaries to benefit from the subsidiary reporting exemption available under the CSRD.

EFRAG has indicated that no final decision has yet been made on the precise design of these options, and the reporting perimeter is expected to be one of the key areas of consultation during 2026.

Does N-ESRS include value chain reporting?

One area that has not changed is the treatment of the value chain.

The proposed N-ESRS continues to include both upstream and downstream value chain impacts.

This means companies will still need to understand and report material impacts connected not only to their own operations, but also to suppliers, business relationships, products and services.

For many organizations, value chain reporting is likely to remain one of the most challenging aspects of compliance, particularly where sustainability data is not yet consistently available across global operations and supply chains.

The retention of value chain reporting requirements also reflects EFRAG’s objective of ensuring that sustainability reports provide a fair presentation of an undertaking’s material impacts.

How does N-ESRS interact with IFRS S1 and IFRS S2?

A key theme throughout the EFRAG presentation was interoperability.

Many non-EU companies already report under IFRS Sustainability Disclosure Standards, particularly IFRS S1 and IFRS S2. EFRAG is therefore seeking ways to minimize duplication and facilitate compliance across multiple reporting frameworks.

The proposals include:

- Alignment of common disclosure content between N-ESRS and IFRS standards

- Potential incorporation by reference to IFRS sustainability reports

- Consultation on practical solutions to avoid double reporting

This is likely to be one of the most closely watched aspects of the consultation process, particularly among multinational groups that have already invested heavily in ISSB-based reporting programs.

While complete alignment is unlikely, EFRAG appears committed to reducing unnecessary duplication wherever possible.

N-ESRS timeline: when will the standards be finalized?

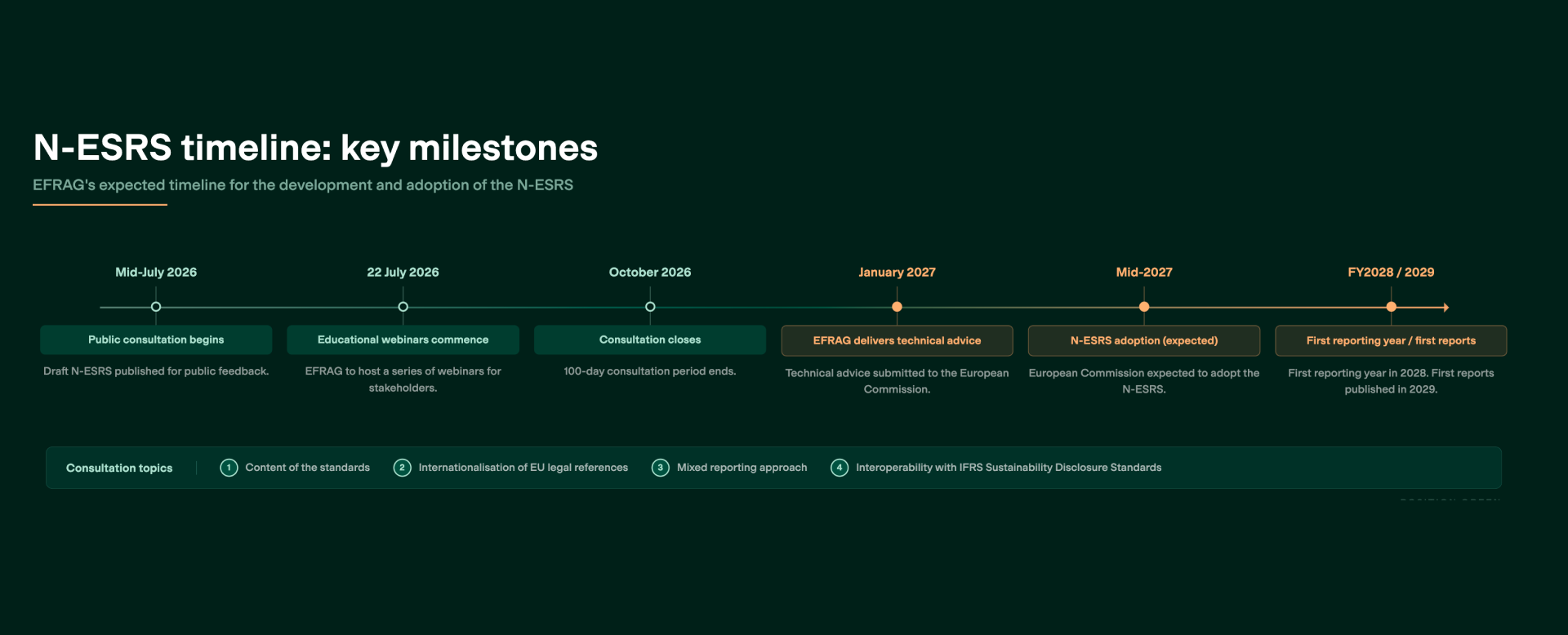

EFRAG plans to launch a public consultation on the draft N-ESRS in mid-July 2026.

The consultation is expected to run for 100 days and will be accompanied by educational webinars, field testing and stakeholder outreach activities.

The current timeline is:

- Mid-July 2026: Public consultation begins

- 22 July 2026: Educational webinars commence

- October 2026: Consultation closes

- January 2027: EFRAG delivers technical advice to the European Commission

- Mid-2027: Expected adoption of the N-ESRS

EFRAG has identified four key consultation topics:

- Content of the standards

- Internationalization of EU legal references

- The proposed mixed reporting approach

- Interoperability with IFRS Sustainability Disclosure Standards

The consultation process will provide stakeholders with the first formal opportunity to influence the final design of the standards before EFRAG submits its technical advice to the European Commission.

Three things that stand out from EFRAG’s proposals

Several aspects of the proposals are particularly noteworthy.

1. The reporting package remains substantial

Despite the removal of double materiality, the N-ESRS still consists of twelve standards covering governance, strategy, policies, actions, metrics and targets.

2. Value chain reporting remains firmly in scope

Many companies hoped that value chain reporting requirements would be significantly reduced. The latest proposals suggest this is not currently the direction of travel.

3. Interoperability has become a strategic priority

The prominence given to IFRS interoperability indicates that EFRAG recognizes the reality facing many non-EU groups. Most companies expected to remain in scope are already navigating multiple sustainability reporting frameworks and will be looking for opportunities to leverage existing disclosures and processes.

What should non-EU companies do now?

The political debate surrounding CSRD and the Omnibus reforms is likely to continue throughout 2026 and beyond.

However, companies that remain within scope of Article 40a should avoid viewing the N-ESRS as a distant or uncertain requirement.

The latest proposals indicate that reporting will still require a structured understanding of sustainability impacts, governance arrangements, policies, actions, metrics and targets.

Companies should therefore use the consultation period to assess:

- Whether they remain within scope following the Omnibus amendments

- Which reporting perimeter option may be most appropriate

- The extent to which existing ESRS or IFRS reporting programs can be leveraged

- Potential value chain reporting challenges

- Opportunities to streamline future compliance through interoperability

- The governance, data and reporting capabilities that may need to be developed ahead of FY2028 reporting

- A high-level roadmap for N-ESRS compliance, including key milestones, resource requirements and implementation priorities

For the approximately 1,200 non-EU companies expected to remain in scope, the consultation period provides an opportunity to assess likely obligations, identify implementation challenges and begin building a roadmap towards FY2028 compliance.

While the standard is not yet final, the direction of travel is becoming increasingly clear.

Don’t wait to take action on your strategic sustainability

For companies likely to remain within scope, the consultation period should be viewed as an opportunity to prepare rather than a reason to delay planning.

This may seem like a lot of information, and in fairness, it is. But you do not need to navigate it all alone. Our team at Position Green makes a habit of staying ahead of all regulatory changes, so you can navigate them with confidence, both in our software and working with our team of advisory experts.

Chat with us

Simon Taylor

Senior Director

Position Green