Fair presentation vs undue cost or effort under the revised ESRS: A key reporting and assurance challenge for 2026

Less attention has been given to another change that may prove just as significant in practice.

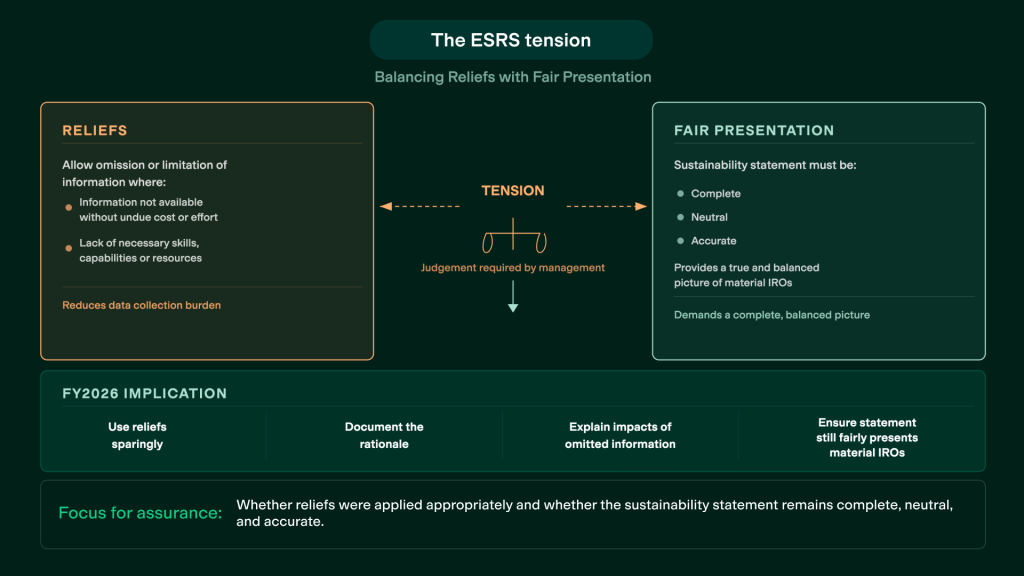

The revised standards strengthen the concepts of fair presentation and faithful representation while also introducing new reliefs for information that is not available without undue cost or effort, or due to a lack of necessary skills, capabilities or resources within the undertaking.

Together, they raise an important question: How can a sustainability statement fairly present a company’s impacts, risks and opportunities if material underlying information has been omitted?

This question sits at the heart of the revised ESRS, but the standards themselves do not establish a bright line between the legitimate use of a relief and a failure to achieve fair presentation.

As a result, greater responsibility shifts to CFOs, sustainability reporting teams and auditors to determine where the boundary lies in practice.

With companies preparing to apply the revised ESRS for FY2026 reporting, the interaction between fair presentation and the new reliefs is likely to become one of the most important questions of the coming reporting cycle.

The revised ESRS introduce significant new reliefs

The revised ESRS contain two important relief mechanisms. The first is based on the availability of information without undue cost or effort. The second is based on the availability of the necessary skills, capabilities or resources within the undertaking.

The relief for undue cost or effort

The revised ESRS introduce a general relief based on the use of “reasonable and supportable information available without undue cost or effort”.

In broad terms, companies are not required to obtain information where doing so would involve undue cost or effort, provided they make use of the reasonable and supportable information that is available to them.

The relief is embedded throughout ESRS 1 and applies to:

- The double materiality assessment;

- The identification of material impacts, risks and opportunities;

- Determining the scope of the value chain;

- Obtaining information from entities in the value chain;

- The preparation of sustainability metrics;

- The reporting of current financial effects; and

- The reporting of anticipated financial effects.

The relief also affects the scope of certain metrics. Where reliable direct or estimated data cannot be obtained for parts of the undertaking’s operations or value chain without undue cost or effort, the undertaking may report a metric on a partial scope rather than covering the entire undertaking or value chain.

Whether a cost or effort is considered “undue” depends on the circumstances of the undertaking. Companies are expected to balance the cost of obtaining information against the usefulness of that information to users of the sustainability statement.

Importantly, the relief is not intended to excuse a lack of effort. Before concluding that information is unavailable without undue cost or effort, undertakings are expected to use all reasonable and supportable information already available or obtainable through reasonable efforts.

Borrowed from IFRS, but applied more broadly

The concept of “reasonable and supportable information available without undue cost or effort” is not new. The wording is drawn from the ISSB Sustainability Disclosure Standards (IFRS S1 and S2) to improve international interoperability.

However, the revised ESRS applies it far more broadly, extending the concept directly into the double materiality assessment and core metrics preparation, areas where the ISSB standards do not explicitly offer it.

The relief for lack of skills, capabilities or resources

The revised ESRS also introduce a targeted relief where an undertaking lacks the skills, capabilities or resources necessary to produce certain information.

This relief is narrower in scope and applies only to quantitative information on anticipated financial effects.

Under ESRS 2, an undertaking is not required to provide quantitative information about the anticipated financial effects of material risks or opportunities if it does not have the skills, capabilities or resources needed to prepare that information.

Unlike the undue cost or effort relief, which focuses on the burden of obtaining information, this relief focuses on the undertaking’s ability to generate the information in the first place.

Fair presentation becomes more important under the revised ESRS

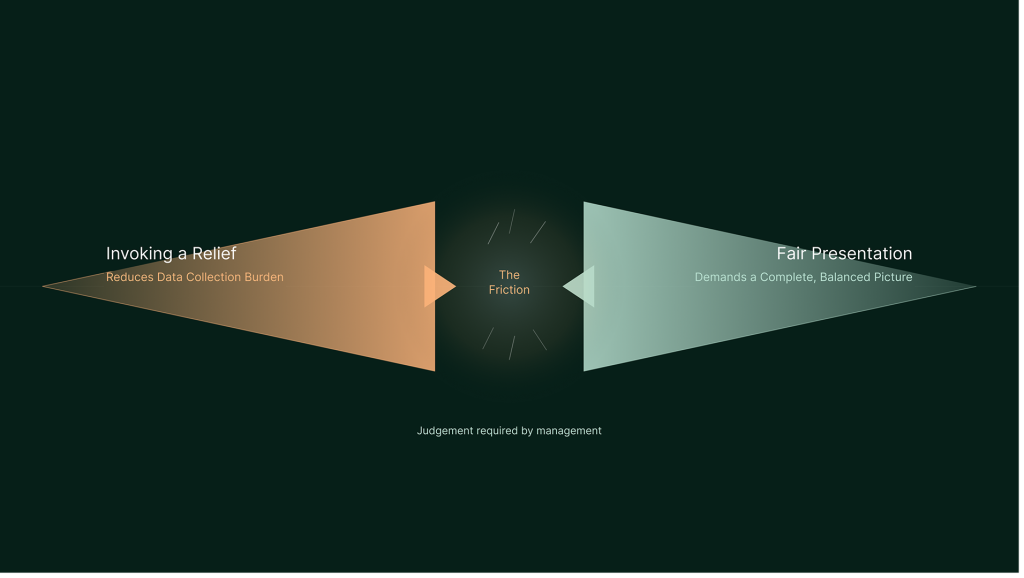

Taken together, the two reliefs give undertakings greater flexibility in determining what information can reasonably be obtained and reported.

Importantly, neither relief has a time limit on its use. An undertaking may continue to omit information because of undue cost or effort, or a lack of skills, capabilities or resources, for as long as the relevant conditions are met.

This was one of the concerns raised by European supervisory authorities during the consultation process. The ECB and ESMA warned that permanent reliefs could reduce comparability, create persistent data gaps for users and weaken incentives to improve sustainability data collection and reporting capabilities over time.

The European Commission chose not to introduce a time limit on the use of the reliefs. This decision increases the importance of fair presentation as an overarching reporting objective.

ESRS 1 paragraph 3 sets out the overall objective of the sustainability statement, taken as a whole: “to present fairly all the undertaking’s material sustainability-related impacts, risks and opportunities and how the undertaking manages them.”

ESRS 1 paragraphs 19 to 21 explain that fair presentation is achieved when sustainability information is relevant and faithfully represented. To be useful to users, the information should also exhibit the enhancing qualitative characteristics of comparability, verifiability and understandability.

Furthermore, ESRS 1 Application Requirement 6 places the burden on undertakings to consider whether the sustainability statement, viewed as a whole, fairly presents their material impacts, risks and opportunities.

The assessment therefore extends beyond compliance with individual disclosure requirements. Fair presentation explicitly depends on faithful representation, which is defined by three characteristics.

What is faithful representation under the revised ESRS?

ESRS 1 describes faithful representation as a complete, neutral and accurate depiction of an undertaking’s material impacts, risks and opportunities.

Appendix B explains what this means in practice. Information should be:

- Complete: it includes the material information users need to understand the nature, extent and significance of an impact, risk or opportunity.

- Neutral: it is presented without bias, manipulation or selective omissions that make the company’s profile appear more favorable.

- Accurate: it is free from material error, with clear explanations of assumptions and sources of uncertainty where estimates are used.

What this means for FY2026 reporting

The revised ESRS give companies more flexibility, but they do not remove the requirement for fair presentation.

This is where the new reliefs become difficult in practice. The standards allow companies to omit, limit or defer certain information where it is not available without undue cost or effort, or where the undertaking lacks the necessary skills, capabilities or resources.

At the same time, the sustainability statement must still provide a fair presentation of the undertaking’s material impacts, risks and opportunities.

The new standards do not draw a bright line between legitimate use of a relief and a failure to achieve fair presentation. That boundary will depend on judgment by management, challenge from auditors and, over time, regulatory practice.

For many companies, FY2026 will be the first reporting cycle under the revised ESRS. Companies should therefore be cautious about treating the new reliefs as a simple mechanism for reducing reporting effort.

A decision to rely on undue cost or effort, or on the lack of skills, capabilities or resources, is ultimately a judgment that will need to be justified to auditors.

Companies should be prepared to demonstrate:

- Why the information could not reasonably be obtained;

- What efforts were made to obtain it;

- What alternative information was considered;

- How the omission affects users’ understanding of the undertaking’s material impacts, risks and opportunities; and

- Why the sustainability statement continues to provide a fair presentation despite the limitation.

For auditors, the challenge is similar.

Auditors will need to assess:

- Whether management’s use of the reliefs is reasonable;

- Whether it is adequately supported by evidence; and

- Whether the resulting sustainability statement continues to provide a fair presentation of the undertaking’s material sustainability matters.

This assessment extends beyond compliance with individual disclosure requirements. ISSA 5000 requires assurance practitioners operating within a fair presentation framework to consider the overall presentation, structure and content of the sustainability information.

This is particularly relevant for FY2026 reporting. The European Commission has not yet adopted formal EU assurance standards for sustainability reporting, and auditors are currently relying on ISSA 5000 and the CEAOB Guidelines on Limited Assurance on Sustainability Reporting.

As a result, some of the early boundaries around fair presentation and the use of these reliefs are likely to emerge through assurance practice before they are addressed through detailed EU assurance standards.

Conclusion: Use careful judgment

The revised ESRS introduce permanent reliefs for information that is unavailable without undue cost or effort, or due to a lack of skills, capabilities or resources.

However, the revised ESRS strengthen the concepts of faithful representation and fair presentation, requiring the sustainability statement to fairly present the undertaking’s material impacts, risks and opportunities.

The boundary between legitimate use of these reliefs and a failure to achieve fair presentation is likely to emerge first through assurance engagements.

As corporate reporting teams map out their strategies for 2026, CFOs and sustainability leads should exercise careful judgment in using these reliefs and be prepared to make the case that the overall statement is fairly presented.

Simon Taylor

Senior Director

Position Green